“The preservation of the republic is no less than governing- what a thankless task it is!”

Cicero, Speech, 9 November 63 BC

India finds itself in a relatively stronger position than many emerging markets amid the current global turmoil. But we are far from immune. The notion that India could somehow decouple from global headwinds was always unrealistic. Our economy is simply too large and deeply integrated into energy markets, supply chains, and capital flows. The recent flare-up in the Middle East has driven this point home forcefully.

Disconcerting Macros – The Challenge and the Response

The macroeconomic picture is clearly darkening. Rising crude prices are feeding into inflation, widening the import bill, and putting pressure on both the current account and fiscal deficit. We are confronting the challenging prospect of twin deficits — fiscal and current account — compounded by inflationary pressures.

Foreign investors have pulled out over $20 billion from Indian equities in the first four months of 2026 — already exceeding the full-year outflow of 2025. The Nifty and Sensex suffered notable declines. What provided some stability was robust buying by domestic institutional investors. For the first time, DII ownership in Nifty-500 companies has surpassed that of foreign investors. This marks a meaningful shift in market dynamics. Markets witnessed sharp corrections, with investor wealth eroding by nearly ₹17 lakh crore in just two trading sessions in mid-May.

Our foreign exchange reserves have come down from $728 billion to around $690 billion as the RBI stepped in to defend the rupee. The current account deficit is likely to widen to around 2.1-2.2% of GDP — not disastrous, but clearly higher than what we’ve been used to. Still, with reserves covering nearly 10 months of imports and GDP growth holding above 6%, we are not in the same fragile territory as 2013.

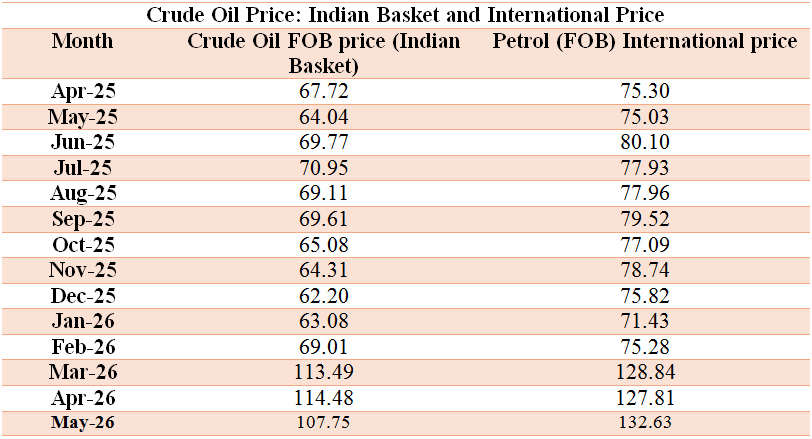

Oil remains the biggest headache. Every $10 rise in crude adds roughly $13-14 billion to our annual import bill. With 85% of our crude imported, we are structurally exposed.

This vulnerability is not uniquely Indian. The instability surrounding the Straits of Hormuz represents a global concern. History offers a warning: when oil approached $140 per barrel in 2008, the outcome was not sustained energy scarcity but global demand destruction, financial crisis, and eventually collapsing oil prices. The concern today is that weakening consumption may emerge sooner.

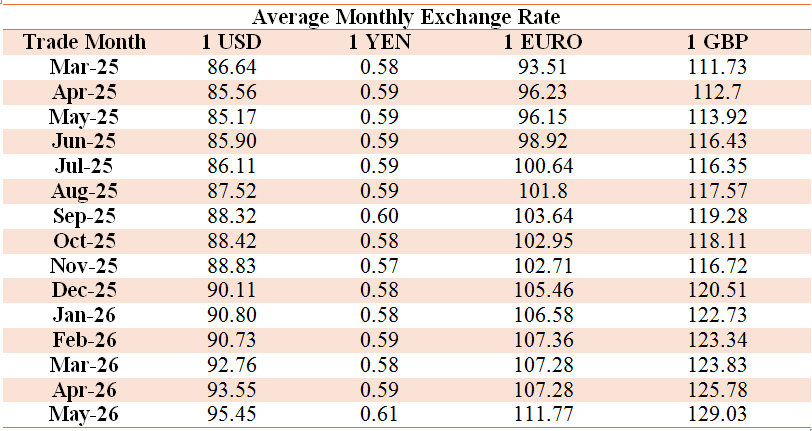

Simultaneously, the rupee — Asia’s weakest-performing currency this year — depreciated to a record low of Rs 95.62 per US dollar, reflecting capital outflows and mounting external pressures.

Inflation risks are also resurfacing. Retail inflation climbed to a four-month high of 3.5% in April 2026, raising concerns about imported inflation through fuel, transport, and food prices. Financial markets, especially energy markets, remain exceptionally sensitive to geopolitical uncertainty. This messy combination of risks feeding into each other is captured poignantly in Muin Ahsan Jazbi’s famous couplet:

“जब कश्ती साबित–ओ–सालिम थी साहिल की तमन्ना किस को थी

अब ऐसी शिकस्ता कश्ती पर साहिल की तमन्ना कौन करे”

When the boat was intact, no one longed for the shore; now that the boat is broken, expecting safe arrival appears futile.

Elevated energy prices are already affecting manufacturing, logistics, aviation, fertilisers, and power generation, threatening industrial output and economic momentum. Simultaneously, rising global uncertainty has triggered classic risk-off behaviour, increasing volatility in Indian equity and debt markets.

Currency depreciation may benefit exports, but it also raises import costs, external borrowing burdens, and corporate debt servicing costs. Consequently, the policy challenge for the RBI is becoming increasingly difficult: maintaining currency stability without excessively tightening liquidity or compromising growth.

Beyond immediate macroeconomic concerns, geopolitics is accelerating fragmentation in the global economic order. Trade realignments, sanctions, supply-chain disruptions, weaponisation of technology, and intensifying strategic competition are reshaping the contours of globalisation.

Indian Scenario

The current global turmoil is not just a short-term shock. It shows that the world economy is changing in fundamental ways. We enter this period from a position of relative strength — solid growth, strong reserves, and a more diversified economy than many peers. Yet our size and integration with the world mean that every major external tremor will be felt at home. The real challenge for policymakers is not merely to manage the crisis, but to use it as a catalyst for long-overdue changes.

I have maintained for nearly three decades that consistent policy direction on investment and structural reforms is not optional; it is a macroeconomic necessity. We must use this period of stress to accelerate the reduction in oil import dependence, diversify supply chains, and enhance export competitiveness.

Crude oil, which briefly dipped below $90 a barrel after early hopes of a quick ceasefire, has since surged back above $106, reflecting an 11-week conflict that both Washington and the markets badly miscalculated.

India has the fundamentals to emerge stronger. However, this will require greater urgency and clarity in policymaking. Symbolic appeals, such as the Prime Minister’s call for reduced consumption, have limited impact unless backed by deeper structural measures. The damage remains reversible for now, but the window of opportunity is narrowing.

Disaggregated Picture

India in May 2026 presents a picture of reasonable macro stability but with emerging stresses on growth, external balances and the currency, against a backdrop of high commodity prices and frothy asset markets. Let us examine some important metrics.

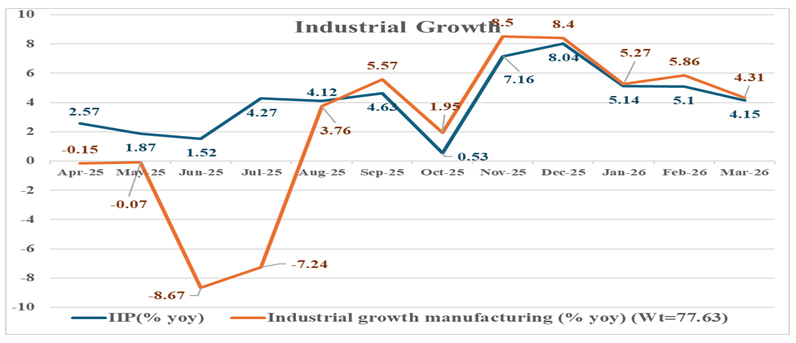

1. Industrial production grew 4.1% in March 2026, down from 5.2% in February. While manufacturing held up reasonably well, electricity growth slowed sharply to 0.8%, reflecting softer energy demand. PMI and GST collections remain supportive, but private investment continues to stay cautious amid global uncertainty. Industrial growth remains vulnerable and lacks broad-based momentum.

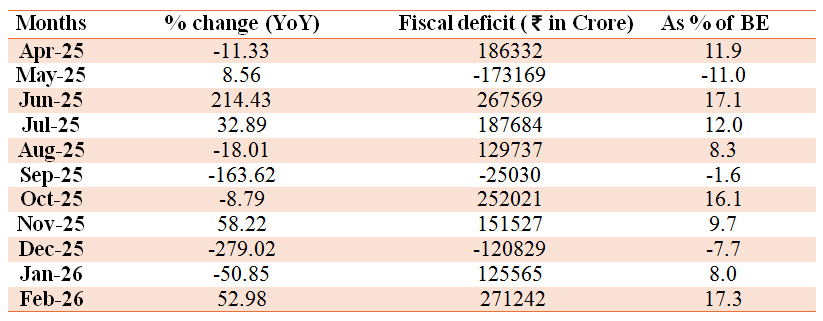

2. Fiscal consolidation is on, with the Centre’s fiscal deficit declining from 9.2% of GDP in FY21 to 4.8% in FY25 and budgeted at 4.4% in FY26. Projections for FY26–27 target a further reduction to around 4.3%, broadly aligned with the medium-term glide path. This improvement has been supported by strong nominal GDP growth, buoyant GST and direct tax collections, restrained revenue spending, and protected capital expenditure. However, rising crude oil prices, subsidy pressures, and weaker external demand threaten fiscal targets. The RBI’s ₹2.87 trillion surplus transfer provides temporary relief by easing borrowing needs. While robust tax revenues and sustained capex support stability, geopolitical risks, imported inflation, and rising welfare commitments may slow consolidation efforts.

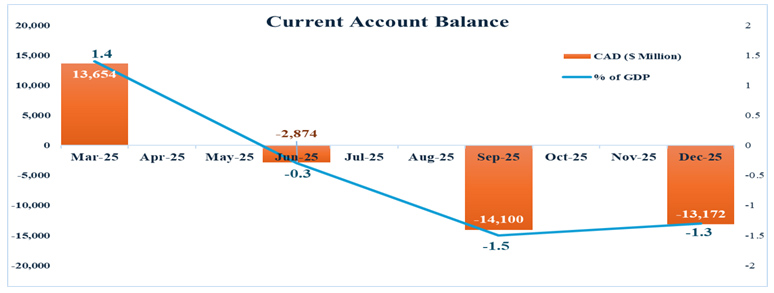

3. The current account deficit (CAD) is widening as India’s trade deficit reached $28.4 billion in April 2026, driven by sharp increases in oil and gold imports. Higher energy prices linked to Middle East tensions have heightened external sector pressures, while resilient non-oil, non-gold imports continue to support demand. Strong services exports, remittances, stable capital inflows, and large foreign exchange reserves provide important buffers. However, persistently high crude prices and growing global fragmentation pose downside risks if exports and growth weaken simultaneously. CAD could rise to around 2.2% of GDP in FY27 from about 0.8% earlier, increasing pressure on the rupee, inflation, and reserves.

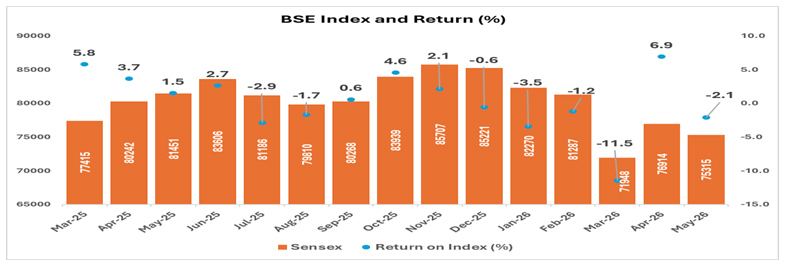

4. BSE Sensex levels in May 2026 reflected heightened volatility and investor caution, fluctuating between 74,000 and 77,500 amid geopolitical tensions, FPI outflows, rising oil prices, and rupee weakness. High valuations and inflation concerns dampen sentiment, particularly in IT and mid-cap stocks. However, strong domestic institutional participation and steady SIP inflows limited deeper corrections. Banking and metal stocks remained resilient, while export-oriented sectors faced demand and currency pressures. Despite short-term volatility, long-term drivers such as domestic consumption, infrastructure spending, and digitalisation continue to support equities. However, stretched valuations and external risks leave markets fundamentally strong but vulnerable to sentiment-driven corrections.

5. The rupee depreciation is symptomatic of a deeper malaise and structural shifts in supply and demand rather than their short-term speculation. The rupee depreciated sharply to record lows near ₹95–96 per US dollar in May 2026, driven by rising crude prices, widening trade deficits, and foreign portfolio outflows. This decline partly reflects a stronger dollar and global risk repricing. A decade of neglecting mining and energy has left us with shortages and skyrocketing prices, just as AI, green tech, and defence spending are booming.

India-specific factors, such as high oil and gold imports and debt outflows, have intensified pressure. Despite foreign exchange reserves of around USD 700 billion providing room for intervention, structural trade deficits and global yield differentials continue to sustain depreciation pressures. There is also the issue of India-US yield spreads, with the difference between India and US interest rates compressing. Since India imports over 80% of its crude requirements, higher oil prices significantly increased dollar demand. Although rupee weakness offers limited export support, it raises imported inflation and highlights India’s continuing external vulnerability. These factors necessitate reduced external debt (constitute 5 % of India’s total external debt), attracting foreign investment, regulation of speculative capital flows, reduced dependence on oil imports, and sustained investment in upskilling and capability development.

6. Brent crude remained near triple-digit levels in late May 2026, trading mostly between $105–120 per barrel and briefly crossing $130 amid geopolitical tensions and supply constraints. For India, a major crude importer, high oil prices pose a significant macroeconomic challenge by increasing import costs, widening trade and current account deficits, and creating fiscal pressures through subsidies and fuel pricing constraints. Expensive oil also complicates the monetary policy trade-off by raising inflation and inflation expectations.

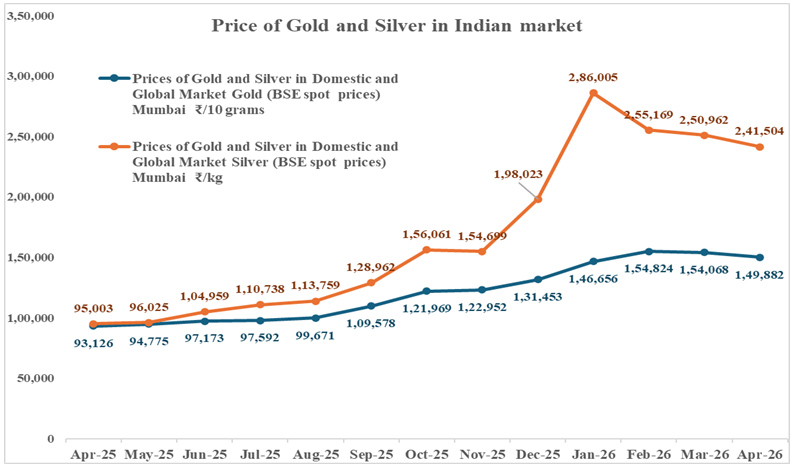

7. Gold prices surged sharply in 2026, reaching around USD 4,520 per ounce by May, while domestic 24-carat prices touched nearly ₹15,700–15,800 per gram, close to record highs. Geopolitical tensions, central bank buying, inflation fears, rupee depreciation, and market uncertainty increased demand for gold as a safe-haven asset. A weaker rupee amplified domestic price gains, encouraging investment in gold ETFs and physical bullion. While rising gold prices supported household wealth and rural balance sheets, they also increased gold imports, worsening trade and current account deficits. The allocation of greater savings towards gold raises concerns about financial intermediation and productive investment. Gold thus reflects both financial security and macroeconomic vulnerability.

8. Silver prices surged in 2026, driven by both safe-haven demand and rising industrial consumption linked to renewable energy, electronics, and solar manufacturing. International prices traded around USD 80–85 per ounce in May 2026 after briefly crossing USD 87, while domestic prices reached nearly ₹266 per gram due to rupee depreciation. Strong inflows into silver ETFs reflected investor demand for inflation protection amid market uncertainty. However, silver remained more volatile than gold because industrial demand is closely tied to global growth expectations. While high prices benefited investors, they also increased import costs and external pressures. Silver remains more speculative than gold, with upside tied to clean energy demand but greater downside risk if growth weakens.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.