Let us examine the monthly contours of the Indian economy in the third article of this monthly series. The Indian economy enters FY26 with sustained momentum, supported by robust domestic demand, policy-driven capital expenditure, and strengthening financial and external buffers. Official assessments highlight “strong economic momentum” and broad-based sectoral performance despite an adverse global environment characterised by tighter financial conditions, geopolitical conflict, and energy price volatility.

The macroeconomic context of resilience after repeated shocks places real GDP growth in the mid-6 to low-7 % range, below the post-pandemic rebound peak but still among the fastest in major economies. Growth projections for FY27 carry “substantial downside” risks due to escalating energy prices, supply-chain disruptions stemming from the Iran–West Asia conflict, and potential spillover effects from advanced-economy policy choices not aligned with India’s priorities.

This contrast between solid current growth and mounting medium-term risk constitutes the macro saga: India has come through a series of difficult shocks, but the cushions that enabled this resilience carried real costs, and they now demand more careful stewardship.

Fiscal deficit: consolidation under stress

India’s fiscal strategy over the last few years has aimed at a gradual “fiscal glide path”, balancing consolidation with growth-supportive public investment. The Union government set a medium-term goal of bringing the fiscal deficit below 4.5 % of GDP by FY26, and targets of around 4.4 % for FY25-26 and 4.3 % for FY26-27 are being met or nearly met. This reflects deliberate restraint on non-capital expenditure and a focus on infrastructure-oriented capex to support potential growth. Yet this consolidation is increasingly challenged by exogenous shocks. The ongoing West Asian crisis and energy-price volatility could raise subsidies on food, fertiliser and petroleum products, exacerbating fiscal pressure. The Finance Ministry has stressed that rationalising non-capex expenditure is critical not only to protect growth-supportive capital outlays but also to avoid fiscal slippages in such an environment.

The fiscal stance, therefore, faces three structural tensions:

- The need to sustain large public capex to crowd in private investment.

- The political and social necessity of subsidies and welfare spending in a period of relative price shocks and uneven labour-market recovery.

- The macro requirement to contain debt and deficit so that India’s risk premia, borrowing costs and currency remain manageable.

So far, India is “relatively better placed” than many emerging peers in managing these near-term fiscal challenges, but the margin for error has narrowed, and the quality of expenditure—capex versus revenue—will be more important than headline deficit ratios.

Current account deficit and external vulnerability

India’s current account deficit (CAD) benefited briefly from lower energy prices and strong services exports, compressing the deficit to below 1 % of GDP in recent years. However, the latest assessments forecast a widening CAD from roughly 0.8% to about 2.2% of GDP as energy imports rise and export growth softens -the “double whammy” of global demand weakness and higher commodity prices.

The West Asian conflict, Iran-related risks, and volatility in crude prices and shipping routes directly affect India’s import bill, rupee trajectory and external balances. As brought out by us, fuel subsidies cushion domestic inflation for now, and diversified energy sourcing eased supply pressures, but these measures shift part of the burden onto fiscal accounts and do not eliminate external risk.

It needs no clairvoyance to perceive that the two “critical imbalances” for India are the current account and the consolidated fiscal account, both likely to come under pressure as global energy and geopolitical tensions persist. The sustainability of a widening CAD will depend on three factors:

- The strength and composition of capital inflows (FDI versus portfolio), which have so far provided adequate financing but remain sensitive to global risk sentiment and domestic policy credibility.

- The competitiveness and diversification of exports, including services, where India has a comparative advantage but faces tariff pressures and strategic trade realignments, notably in the US and other advanced economies.

- The rupee’s managed flexibility; higher oil prices and CAD widening tend to exert depreciation pressure, though reserves and intervention policy can limit disorderly moves at some fiscal and monetary cost.

While India’s external position remains more robust than during earlier episodes of “twin deficit” stress, the room to absorb persistent high oil prices and global fragmentation without policy adjustment is limited.

Inflation: from chronic high to fragile stability

India’s inflation trajectory over the last decade has notably improved. Between 2013 and 2026, headline inflation fell from above 10% to around 3.4%, supported by prudent monetary policy, supply-side reforms, and changes in administered prices, including cheaper telecom services. The inflation-targeting framework and RBI’s incremental tightening during high-inflation phases have anchored expectations more effectively than in previous cycles.

However, recent and prospective shocks have reintroduced uncertainty. The Finance Ministry, even in earlier reports, acknowledged near-term challenges in “reining in inflation” alongside fiscal and external risks, emphasising coordination between monetary tightening and fiscal measures such as duty cuts and targeted subsidies. The current energy shock raises the risk of inflation breaching the comfort zone, particularly through fuel and transport costs and second-round effects on food and core prices.

At present, India’s inflation is “historically low” relative to its own past and moderate by emerging-market standards, but this stability partly reflects policy cushions, viz., fuel subsidies, duty reductions, and intervention, which themselves feed back into fiscal strain. But as I have repeatedly demonstrated over the years in my papers, interviews and speeches, there is a compelling need to sustain low and stable inflation without excessive reliance on fiscally expensive price-smoothing mechanisms, and to allow relative prices to adjust while protecting vulnerable households.

Growth strategies: drivers and fault lines

Despite these constraints, several structural drivers underpin India’s medium-term growth narrative: demographic advantage, rising urbanisation, digitalisation and expanding infrastructure networks. The Economic Survey highlighted broad-based sectoral performance and strengthening labour-market indicators, suggesting that post-pandemic scarring is being gradually reduced.

Key elements of the current growth strategy include:

- Public capital expenditure in transport, logistics, and urban infrastructure aimed at lowering transaction costs and crowding in private investment, particularly in manufacturing and construction.

- Reform and formalisation in tax administration (GST, digital compliance) and finance (UPI, digital lending), which widen the tax base, enhance efficiency and support productivity gains.

- Strategic trade and investment diplomacy, including engagement in new trade arrangements with major partners such as the US, to maintain export growth despite tariff and geopolitical frictions.

However, this growth strategy faces several fault lines:

- High reliance on public capex, which may be harder to sustain if fiscal space narrows due to rising subsidies and interest costs.

- Geopolitical fragmentation that may constrain export-led manufacturing strategies and force India to navigate complex trade-offs between strategic autonomy and access to markets and technology.

- Uneven labour-market gains and the need for more employment-intensive growth, particularly in manufacturing and modern services, to convert demographic potential into broad-based income growth.

These tensions suggest that resilience has been achieved through a specific combination of domestic demand, public investment and relatively stable inflation, but the configuration may not be indefinitely replicable without further structural reforms.

Policy roadmap: managing twin deficits and sustaining growth

Looking ahead, a credible roadmap must simultaneously address fiscal and current account pressures, preserve inflation stability, and sustain growth. Several policy directions emerge:

- Fiscal discipline with expenditure reprioritisation

The emphasis of the Finance Ministry, as also unmistakably brought out by me, on rationalising non-capex expenditure suggests a strategy of protecting high-multiplier infrastructure spending while trimming low-impact subsidies and administrative spending. Strengthening targeted transfers, improving subsidy delivery efficiency (food, fertiliser and fuel), and reducing leakage can help contain the fiscal deficit even in a high energy-price environment. - External-sector resilience and energy strategy

With the CAD expected to widen to over 2 % of GDP under current projections, policy must focus on reinforcing external buffers—reserves adequacy, prudent external borrowing, and stable FDI flows. Continued diversification of energy sources, long-term contracts, and acceleration of renewables can gradually reduce the sensitivity of external balances to oil shocks, though such transitions take time. - Monetary–fiscal moving in tandem to manage inflation

India’s recent success in moderating inflation was built on coordinated action: repo hikes, liquidity withdrawal, and simultaneous fiscal measures like duty cuts and targeted subsidies. Preserving the credibility of the inflation-targeting framework while allowing for calibrated, temporary fiscal interventions during supply shocks are important to avoid unanchored expectations. - Structural reforms for investment and jobs

To make growth more durable and employment-intensive, reforms in land, labour, logistics and regulatory regimes remain central. While many of these are politically demanding, incremental improvements in ease of doing business, contract enforcement, and skilling can cumulatively boost private investment and export competitiveness, thereby alleviating pressure on the current account. - Geopolitical risk management and trade diversification

New trade tensions and strategic competition require India to hedge by diversifying markets, deepening South–South trade links and selectively aligning with advanced-economy supply-chain initiatives where they support domestic industrialisation. Such a strategy can help sustain export growth even as some traditional markets become more contentious or protectionist.

Critical appraisal: “weathered storms”, but at what cost?

The Indian economy has “weathered difficult storms”: real GDP has not only recovered pre-pandemic levels but maintained robust growth despite global headwinds; inflation is far below its chronic double-digit past; and external and financial buffers have strengthened. In comparative perspective, India is “better placed” than many emerging economies to manage near-term shocks. Yet it’s not always realised- much less felt- that the resilience has been achieved through a delicate and evolving policy mix with doubtful sustainability. Fiscal consolidation has progressed but is now imperilled by rising subsidy demands; CAD compression is reversing under energy shocks; inflation stability leans partly on subsidies and administrative measures that create future fiscal liabilities.

A serious assessment must, therefore, distinguish between cyclical strength and structural robustness. Cyclical strength is visible in current growth and inflation numbers; structural robustness will depend on whether India can maintain a prudent twin-deficit trajectory, deepen productivity-enhancing reforms, and navigate geopolitical fragmentation without excessive macro volatility.

In this sense, the Indian economy has not only weathered storms but also accumulated new forms of conditional vulnerability. As I have held on multiple occasions, the roadmap ahead will be judged by its ability to convert present resilience into sustainable, inclusive growth rather than simply surviving the next shock.

Disaggregated Picture

India in May 2026 presents a mixed picture. Let us examine some important metrics for a comprehensive assessment and perspective.

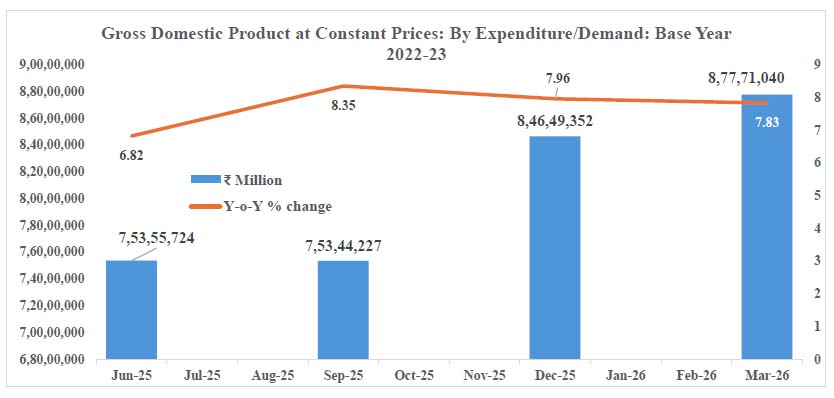

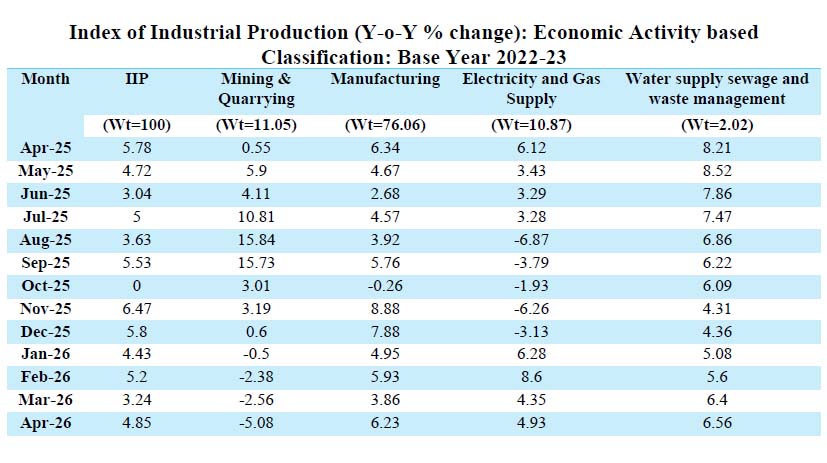

1. Industrial Growth

India’s industrial sector entered FY2026–27 on a positive but moderating trajectory, reflecting a phase of steady expansion rather than rapid acceleration. Industrial growth slowed to 4.9% in April 2026 from 5.7% a year earlier, with the deceleration concentrated in mining and primary goods. However, the underlying investment cycle remains resilient. Capital goods recorded double-digit growth for six consecutive months, while infrastructure and construction goods continue to expand by over 7%, highlighting sustained public capital expenditure and infrastructure spending. The Index of Eight Core Industries also grew a modest 1.7%, led by cement, steel and electricity, signalling a relatively soft start to the fiscal year.

Business activity remains expansionary, though the Composite PMI indicates slower growth in both manufacturing and services, accompanied by weakening business confidence amid softer domestic demand, global trade tensions and geopolitical uncertainty. Additional headwinds include subdued export demand, cautious private investment, delayed monsoon conditions and volatility in energy markets. The slowdown is, however, cyclical rather than structural. Government capital expenditure, Production Linked Incentive (PLI) schemes, infrastructure investments and resilient domestic consumption continue to underpin industrial activity. Sustaining momentum will require stronger private investment, improved logistics, enhanced MSME credit and greater export competitiveness. The near-term outlook remains favourable, provided oil prices remain stable and geopolitical risks do not intensify.

Note: The 2022–23 base year IIP series has been used instead of the 2011–12 series because it better reflects the current structure of India’s industrial economy. The revised series incorporates updated industry weights, a revised product basket, and changes in manufacturing patterns that have occurred over the past decade. As a result, it provides a more accurate measure of present-day industrial activity and growth trends.

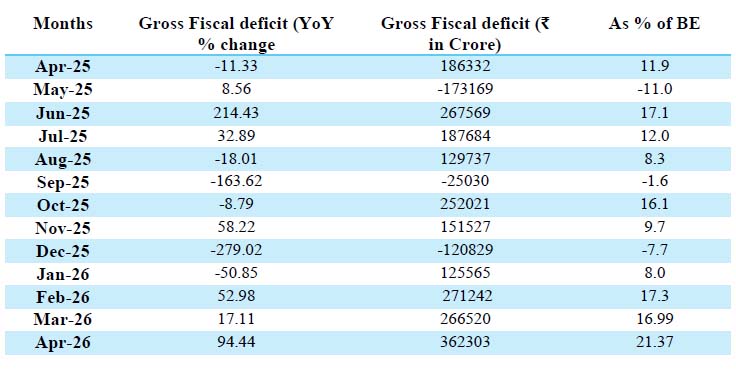

2. Fiscal Deficit

India’s fiscal position remained broadly stable in June 2026, reflecting continued fiscal consolidation while balancing growth, welfare and political-economy priorities. In April 2026, the fiscal deficit stood at 21.4% of the annual Budget target, broadly in line with seasonal spending patterns. Strong tax collections, higher non-tax revenues and prudent expenditure management supported the improvement. The Government continued to prioritise capital expenditure on transport, railways, roads, energy and digital infrastructure, while keeping revenue expenditure under control, thereby strengthening long-term growth without significantly compromising fiscal sustainability.

The Centre has reduced the fiscal deficit from the pandemic peak of 9.2% of GDP in FY21 to 4.8% in FY25, budgeted 4.4% for FY26 and projected 4.3% for FY27. This consolidation has been driven by robust nominal GDP growth, buoyant revenues and sustained public investment rather than expenditure compression. However, fiscal risks persist. Higher defence spending, welfare commitments, subsidy pressures, weaker disinvestment receipts and slowing global growth could constrain future consolidation. Although lower interest rates have eased debt-servicing costs, the projected FY27 deficit of ₹16.96 lakh crore keeps borrowing requirements elevated. The challenge ahead is to preserve fiscal discipline while financing infrastructure, defence and social priorities in an increasingly uncertain global environment.

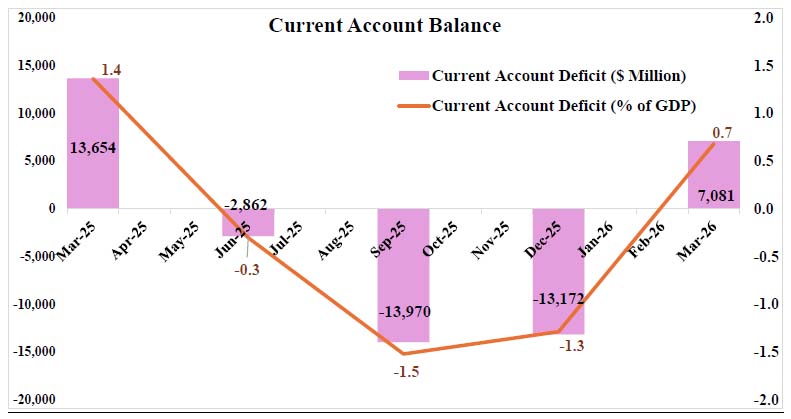

3. Current Account Deficit (CAD)

India’s external sector remained broadly stable during June 2026, with the current account deficit (CAD) staying low but vulnerable to commodity price and geopolitical shocks. The RBI reported a current account surplus of US$7.1 billion (0.7% of GDP) in the January–March 2026 quarter, driven by robust software and services exports, strong remittances, and foreign exchange swap operations. However, for FY2025–26, India recorded a modest CAD of about 0.6% of GDP (US$25.2 billion), broadly unchanged from the previous year and well below historical stress levels. Despite this resilience, structural vulnerabilities persist. India imports nearly 85% of its crude oil, while dependence on electronics and capital goods continues to keep the merchandise trade deficit elevated. Strong domestic demand and infrastructure-led investment have further supported import growth. The CAD has remained manageable primarily because of sustained surpluses in information technology, business and financial services exports, along with record remittance inflows, rather than any structural reduction in import dependence.

Looking ahead, renewed tensions in West Asia and higher global crude prices could widen the CAD during FY2026–27. Nevertheless, ample foreign exchange reserves, stable capital inflows and a diversified export base provide important buffers. Strengthening export competitiveness and reducing energy import dependence remain key policy priorities.

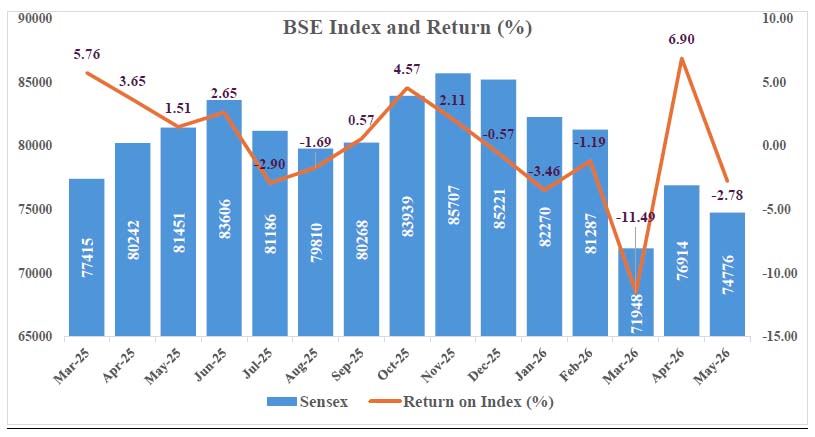

4. BSE Levels

The BSE remained volatile during June 2026, reflecting a market supported by strong domestic fundamentals but increasingly sensitive to global developments and valuation concerns. After extending its post-2023 rally on easing crude oil prices, moderating inflation expectations and expectations of further monetary easing, the market corrected in the third week of June. The BSE Sensex, trading around 77,100 on 26 June 2026, remained close to record highs, underscoring India’s growth premium relative to many emerging markets. Optimism was driven by expectations of robust GDP growth, resilient corporate earnings, healthy bank balance sheets, sustained infrastructure spending and rising domestic institutional investments, particularly through systematic investment plans (SIPs). However, elevated valuations have increased market vulnerability to external shocks. Investor sentiment remained highly responsive to geopolitical tensions in West Asia, US Federal Reserve policy signals, global capital flows and quarterly earnings announcements. Although foreign portfolio flows turned volatile, strong domestic liquidity continued to provide a cushion. Sector-specific corrections indicated selective profit booking and stock re-rating rather than a broad-based market reversal. Overall, June represented a phase of healthy consolidation within a continuing long-term bull market. Going forward, sustained economic growth, stable inflation and lower crude oil prices are likely to support equity markets, although rich valuations warrant greater caution against global risk-off episodes.

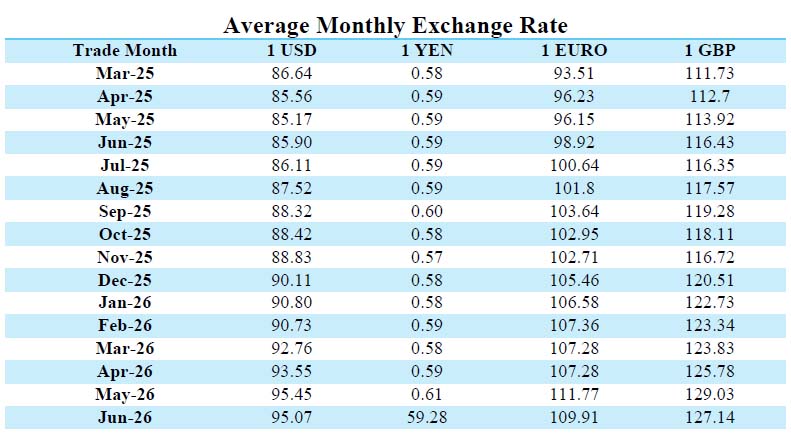

5. Rupee Movement

The rupee remained under pressure during June 2026, trading in a historically weak range of ₹94.3–94.5 per US dollar, although the depreciation was gradual and well managed rather than disorderly. After weakening through much of the month, the currency appreciated by nearly 1% in the final week of June, emerging as one of Asia’s better-performing currencies, supported by softer crude oil prices, renewed foreign portfolio inflows, and timely intervention by the RBI. With an average exchange rate of around ₹94.4 (high of ₹95.8, low of ₹92.7), volatility remained contained despite the overall depreciation trend. The rupee’s movement reflected a manageable current account deficit, sustained by robust services exports and capital inflows, while the RBI allowed measured depreciation to preserve external competitiveness and conserve foreign exchange reserves. A weaker rupee provided modest support to exports and partly offset imported disinflation from lower oil prices. However, it also heightened medium-term risks of imported inflation if crude oil prices, fertiliser costs, capital goods imports, or US bond yields rise. Overall, the rupee’s performance in June is best characterised as a controlled weakening, broadly consistent with India’s external and monetary policy framework. Its outlook for the remainder of FY 27 will be a function of global oil prices, US Federal Reserve policy, capital flows, and the strength of India’s external balance.

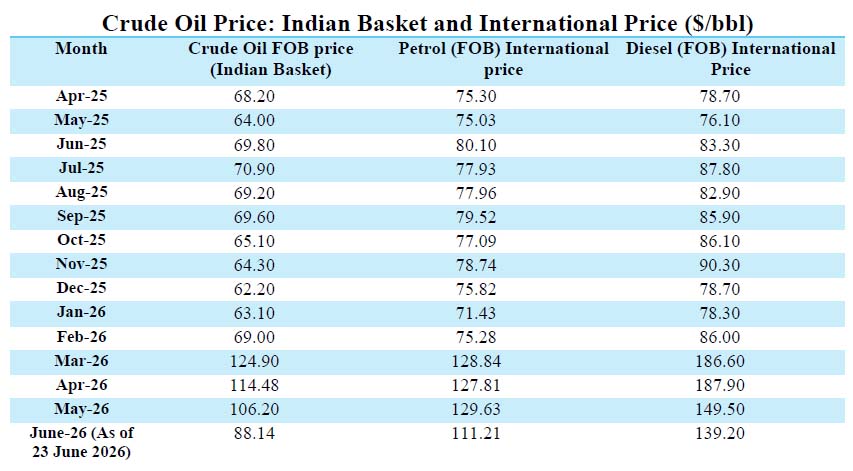

6. Price of Oil

Oil prices declined significantly during June 2026, providing a favourable macroeconomic environment for India, although the relief appears cyclical rather than structural. Brent crude fell to around USD 72 per barrel by 26 June, over 4% lower than the previous day and nearly 22% below earlier peaks, reflecting weaker global demand, easing supply concerns, and downward revisions in price forecasts. The decline placed prices well below the USD 82–85 per barrel range assumed by the RBI and IMF, offering India a welcome buffer against external shocks. Lower crude prices reduced the oil import bill, strengthened the current account position, eased inflationary pressures, and created room for stable retail fuel prices, particularly important for an economy that imports nearly 85% of its crude oil requirements. However, the improvement should be viewed cautiously, as it depends on temporary market conditions rather than a lasting shift in global energy markets. Geopolitical tensions, OPEC+ production decisions, or a recovery in global demand could quickly reverse the trend. Consequently, India continues to diversify crude import sources, expand strategic petroleum reserves, and accelerate renewable energy, ethanol blending, and electric mobility to reduce long-term import dependence. Overall, the decline in oil prices during June substantially strengthened India’s short-term macroeconomic outlook by supporting growth, moderating inflation, and improving external sector stability.

7. Gold Prices

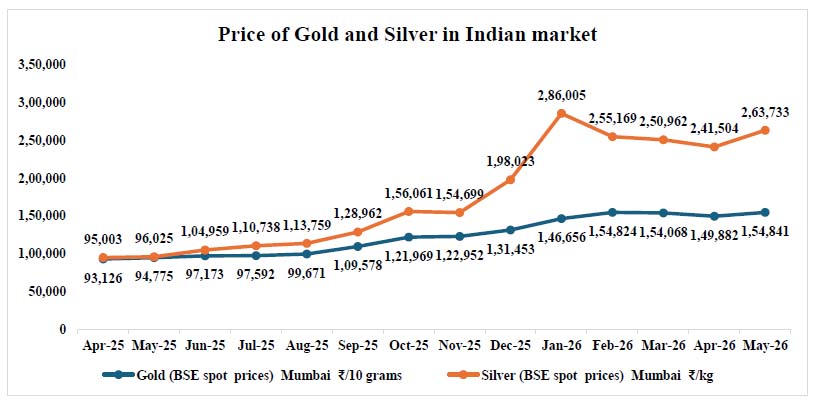

Gold prices remained elevated throughout June 2026, reflecting persistent global uncertainty, geopolitical tensions, and strong safe-haven demand. Domestic 24-carat gold prices fluctuated between about ₹12,500 and ₹13,800 per gram during the month before rising to around ₹14,395 per gram by late June, supported by a weaker rupee and firm international bullion prices.

Internationally, expectations of lower US interest rates, continued central bank gold purchases, and tensions in West Asia sustained prices near record highs. In India, high prices dampened jewellery demand but boosted investment through gold exchange-traded funds (ETFs), while sovereign gold bonds purchased earlier continued to offer attractive returns.

Elevated gold prices also widened India’s merchandise trade deficit by increasing the import bill, thereby exerting pressure on the current account deficit (CAD). The Economic Survey’s observation of a more than 27% year-on-year rise in gold imports highlights households’ preference for gold as both a store of wealth and a hedge against uncertainty, despite higher prices. From a macroeconomic perspective, this reflects risk-averse sentiment and a diversion of household savings from productive financial assets. Gold prices are likely to remain firm if geopolitical tensions persist and global monetary policy continues to ease.

8. Silver Prices

Silver prices remained elevated in June 2026, although gains were more moderate than gold, reflecting both industrial demand and safe-haven buying. International spot silver traded around USD 59 per ounce by late June, fluctuating within a USD 55.7–59.5 range. In India, a weaker rupee and firm global prices pushed retail silver prices to about ₹240 per gram (₹2.4 lakh per kilogram), keeping domestic prices near historic highs.

Unlike gold, silver derives value from both investment demand and extensive industrial use. Strong global demand from the renewable energy, electric vehicle, semiconductor and electronics sectors, particularly the expansion of solar photovoltaic manufacturing, continued to support prices. Investors also viewed silver as an attractive alternative to gold because of its lower cost and stronger industrial demand outlook.

For India, elevated silver prices present mixed implications. They benefit investors, traders and refiners but increase input costs for jewellery manufacturers and industrial users. Higher silver imports also add to the merchandise trade deficit, although the impact remains smaller than gold. Despite some consolidation during the month, prices stayed historically high, reflecting resilient global demand. Going forward, silver prices are expected to remain volatile, influenced by global manufacturing activity, clean energy investments, monetary policy and overall investor sentiment.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.