The Chief Economic Adviser’s (CEA) March Economic Review provides a timely snapshot of India’s macroeconomic health at the end of the financial year. It describes an economy that remains fundamentally resilient but increasingly vulnerable to global headwinds, particularly geopolitical tensions and rising commodity prices. The tone has clearly shifted from complete confidence to cautious realism: domestic fundamentals stay solid, but external disruptions are now beginning to impact growth momentum and expectations.

Transmission Mechanism

A central concern in the Review is the fourfold transmission of global shocks: supply chain disruptions (especially in oil, gas, fertilisers, and exports), rising import prices, higher logistics costs, and the risk of lower remittances from overseas workers. These channels neatly underline how, despite relative macroeconomic stability, India is far from insulated from external developments. Policy, therefore, must walk a tightrope between shortterm cushioning of shocks and longterm structural strengthening.

Growth: Strong, yet Uneven

India continues to rank among the fastest-growing major economies, supported by robust domestic demand, significant public capital expenditure, and a buoyant services sector. GDP growth remains healthy, with recent quarterly numbers showing sizeable contributions from both manufacturing and services. Yet the Review itself acknowledges rising downside risks to the projected 7–7.4 % growth range, mainly from geopolitical uncertainty and energy price volatility.

A closer look reveals some structural concerns. Growth is uneven and heavily skewed towards government spending, with private investment still not firing on all cylinders. Urban consumption is holding up well, but rural demand is lagging, reinforcing the sense of a “Kshaped” recovery. Manufacturing has improved, but this has not yet triggered a broad-based private investment cycle. Employment creation, particularly for the youth, remains inadequate, signalling that current growth is still not sufficiently labourabsorbing. The impact of favourable base effects is also beneficial to the current growth picture. This raises a critical question: is the recovery truly broad-based and sustainable, or still dependent on cyclical and statistical factors?

High-Frequency Indicators: A Mixed Picture

High-Frequency Indicators: A Mixed Picture

High-frequency indicators send out somewhat mixed signals. On the supply and logistics side, measures such as e-way bills and purchasing managers’ indices (PMIs) are showing signs of moderation, reflecting the early impact of rising input costs and heightened uncertainty. In contrast, several demand-side indicators remain reasonably upbeat: vehicle sales and digital transactions continue to expand, especially in urban and formal segments. Rural indicators point to a more fragile reality. Consumption is improving but remains highly sensitive to price movements and income shocks. Overall, the high-frequency data suggest an economy transitioning from a phase of strong post-pandemic recovery to a more uncertain phase in which external shocks are starting to temper the pace of activity.

Inflation: Cooling, but Not Comfortably

Headline inflation has moderated, helped by earlier monetary tightening and somewhat better supply conditions. Yet the comfort is, at best, qualified. Food inflation remains volatile, driven by weather disturbances and structural inefficiencies in the supply chain. Core inflation has eased but is still elevated, particularly in services. The sharp rise in global crude oil prices is a major worry. It pushes up input costs across sectors and creates a classic policy dilemma: tighter monetary policy can curb inflation but risks dampening growth. Added to this is the persistence of structural issues in food supply chains, which complicates the task of durable inflation management and raises the risk of repeated food price shocks.

Fiscal Position: Better, but Still Constrained

Fiscal Position: Better, but Still Constrained

On the fiscal front, there has been visible progress. The deficit numbers are broadly aligned with stated consolidation paths, and tax revenues—both GST and direct taxes—have been robust. The government’s emphasis on capital expenditure is a clear positive, supporting infrastructure buildout and medium-term growth.

Important constraints, however, remain. Revenue expenditure, especially on subsidies and welfare schemes, is still high and constrains fiscal flexibility. Public debt levels are elevated, and interest payments absorb a large share of government revenues. Moreover, the fiscal stress at the state level is neither uniform nor fully reflected in aggregate central assessments. Sustained fiscal consolidation will require a sharper focus on the quality of expenditure, stronger and more stable tax buoyancy, and a renewed push on deeper structural reforms.

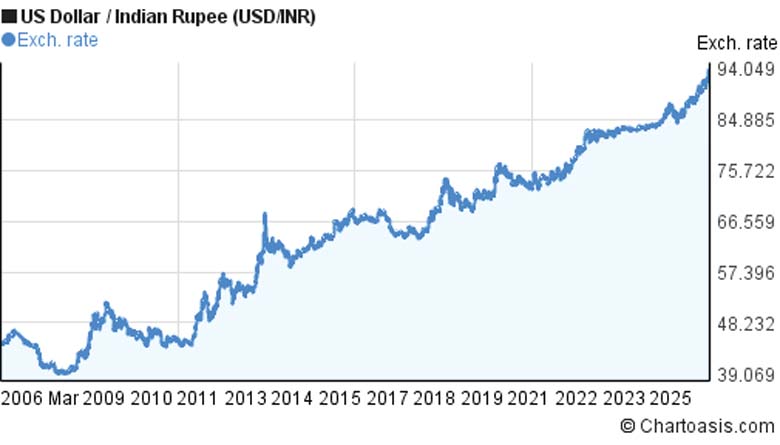

External Sector: Stable, Yet Exposed

The external sector currently appears reasonably stable, with a manageable current account deficit and adequate foreign exchange reserves. Services exports, particularly IT and related services, remain a critical pillar of strength. However, underlying vulnerabilities persist.

Merchandise exports are facing weak global demand, and India’s high dependence on imports of crude oil, electronics, and critical intermediates leaves the economy exposed to price and supply shocks. Capital flows have become more volatile under the influence of global monetary tightening, and although reserves provide a buffer, the currency remains sensitive to sudden changes in risk sentiment.

Investment and Infrastructure: Public-Led, Private Cautious

Investment and Infrastructure: Public-Led, Private Cautious

Infrastructure investment continues to play a central role in sustaining growth, with the public sector leading the charge. Large-scale spending on roads, railways, and other physical infrastructure has helped support activity even as global conditions have turned adverse. The problem is that private investment remains guarded.

Global uncertainty, demand unpredictability, and persistent structural bottlenecks—ranging from land acquisition and regulatory complexity to uneven state-level governance—continue to hamper a more broad-based investment cycle. Public investment can anchor growth for some time, but a durable expansion ultimately requires significantly stronger private sector participation.

Structural Reforms: On Track, but Too Slow

The reform agenda, broadly speaking, is moving in the right direction. Digitalisation, financial inclusion, and production-linked incentive schemes are supporting industrial and services growth. Yet the implementation gaps are still considerable. Progress on key factor market reforms, particularly in labour and land, has been slow and uneven. Small and medium enterprises continue to grapple with limited credit access, regulatory burdens, and patchy digital infrastructure. If India is to unlock meaningful productivity gains and strengthen its global competitiveness, both the pace and depth of structural reforms will need to be stepped up.

Key Limitations of the March Review

While the March Review is informative and generally balanced, it is not without important limitations:

- It does not offer quantified alternative scenarios for growth under different global conditions, which reduces its value for forward-looking policy planning. • Sectoral and distributional impacts are not sufficiently fleshed out, making it hard to see which sectors and population groups are most vulnerable.

- The treatment of inflation is somewhat thin, particularly on possible second-round effects and the precise nature of policy trade-offs.

- The fiscal strategy lacks granularity on how exactly fiscal space will be created and prioritised in the face of competing demands.

Policy Priorities: The Road Ahead

To sustain growth and macroeconomic stability in this more challenging environment, the policy agenda will need to be multi-pronged:

To sustain growth and macroeconomic stability in this more challenging environment, the policy agenda will need to be multi-pronged:

- Short-term support: Provide targeted relief to vulnerable households and to stressed segments, such as MSMEs and energy-intensive industries.

- Fiscal discipline: Maintain consolidation while protecting high-impact capital expenditure and rationalising poorly targeted subsidies.

- Inflation management: Strengthen agricultural supply chains, improve storage and logistics, and diversify energy sources to reduce vulnerability.

- Private investment revival: Enhance policy certainty, streamline regulations, and further improve the ease of doing business.

- External resilience: Diversify export markets and baskets, reduce critical import dependencies, and deepen domestic manufacturing.

- Financial stability: Further strengthen banking and non-banking sectors, deepen capital markets, and enhance systemic risk monitoring.

- Structural reforms: Accelerate reforms in labour, land, and judicial processes to raise productivity and reduce transaction costs.

- Data and transparency: Improve the granularity, timeliness, and accessibility of economic data, and incorporate scenario-based analysis in future official reviews.

Conclusion: From Resilience to Renewal

The March Review captures an economy at an inflexion point. India’s macroeconomic fundamentals remain relatively strong, but the external environment has turned more hostile, and structural constraints at home are asserting themselves more visibly. Growth, though still robust by global standards, is showing early signs of moderation, while inflation risks are resurfacing. The underlying message, as repeatedly demonstrated by us, is that resilience, while necessary, is no longer sufficient.

Gazing at the crystal ball suggests that sustaining high growth will require a decisive shift from a predominantly public-sector-led model to a more balanced one, driven by private investment, deeper structural reforms, and genuinely inclusive development. Policymakers will have to focus not just on preserving growth, but on improving its quality, sustainability, and resilience in an increasingly VUCA (volatile, uncertain, complex, and ambiguous) world. Difficult but doable.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.