Three years of cuts during Ukraine, seventy-six days of absorption during Hormuz, and the contrast with the rest of the world. The government has done well to create an architecture that while paying for past liabilities, it has ensured consumer protection, kept prices in check, kept inflation within limits, and kept the wheels of the economy running. Here is a narrative culled out of media reports, that presents an enabling government that has worked well for the people.

1. The only major economy to cut retail fuel prices through both energy crises

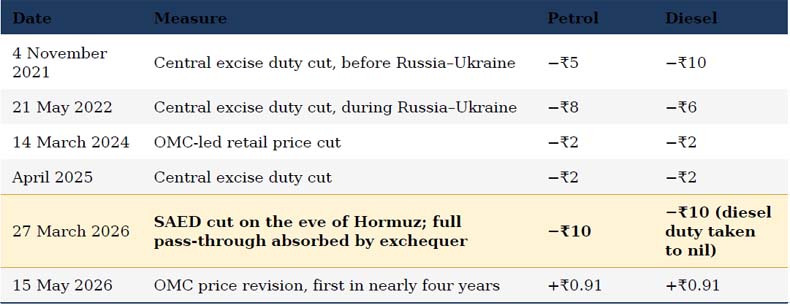

Between the Russia–Ukraine war that began in February 2022 and the Hormuz disruption that began in February 2026, the international price of crude oil has been through two of the sharpest disturbances since the 1970s. Brent has crossed one hundred and twenty dollars a barrel twice in that window. Every major importing economy in the world has passed on the cost to its consumers, in some cases several times over. India has done the opposite. Across the same four years the Indian government has cut the retail price of petrol and diesel four times, the last of those cuts coming on the eve of the Hormuz disruption itself.

Source: PIB releases and OMC notifications. Petrol and diesel duty under the central excise framework comprises Basic Excise Duty, Special Additional Excise Duty (SAED), Road and Infrastructure Cess, and Agriculture Infrastructure and Development Cess. The 27 March 2026 cut was effected on the SAED component.

Through the Russia–Ukraine window, India was the only G20 economy to reduce the retail price of petrol and diesel. The November 2021 and May 2022 cuts together took eighteen rupees off petrol over six months and sixteen rupees off diesel. Through the Hormuz disruption, the SAED cut of 27 March 2026 reduced petrol excise to three rupees a litre and took diesel excise to zero. The pass-through of higher crude was not made to the consumer; it was absorbed by the exchequer.

2. SAED cut and oil bonds: two opposite ways to absorb a price shock

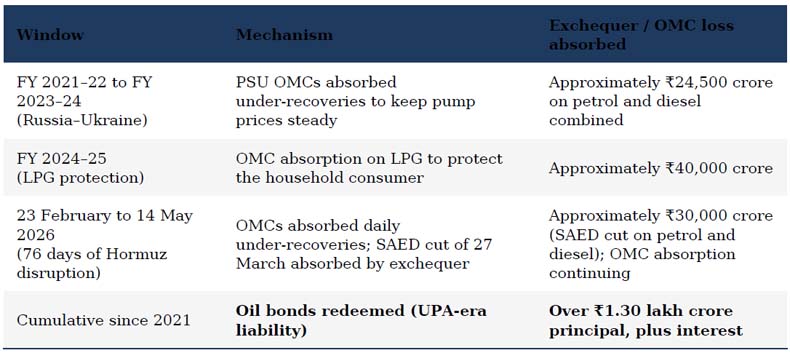

Looking back at the pre-NDA era, it has been argued that petrol cost roughly ₹71 a litre in May 2014 and costs roughly ₹95 a litre today, and presents the difference as evidence of over-taxation. The argument depends entirely on what one thinks the May 2014 number actually represented. It was not the cost of supplying a litre of petrol. It was the price that resulted after the UPA had issued approximately one lakh thirty-four thousand crore rupees in oil bonds to public sector oil marketing companies in lieu of price pass-through, between 2005 and 2010. The 2014 price was a deferred tax invoice on the next generation of consumers.

The Modi government has been redeeming those bonds: roughly ten thousand crores in FY 2021–22, thirty-one thousand one hundred and fifty crores in FY 2023–24, fifty-two thousand eight hundred and sixty crores in FY 2024–25, and thirty-six thousand nine hundred and thirteen crores in FY 2025–26, alongside cumulative interest running into the tens of thousands of crores. The price the Congress nostalgically quotes was being paid by the present government, on behalf of the previous one, until very recently.

The mechanism the present government has used to absorb a price shock is different in kind. When crude rose in 2022 and again in 2026, the central excise duty on petrol and diesel was cut. The reduction was direct, transparent, on-budget, and visible at the pump within a day. The exchequer accepted the loss of revenue. No bond was issued, no obligation was deferred, no future taxpayer was committed to repaying anything. The 27 March 2026 SAED cut alone has cost the central exchequer approximately thirty thousand crore rupees in the current fiscal year. The difference between the two mechanisms is not a matter of optics. It is the difference between paying for a price shock now and pretending to.

3. Losses incurred and compensation borne

At peak Brent of around one hundred and twenty-six dollars a barrel during the Hormuz disruption, the Government of India was absorbing approximately twenty-four rupees a litre on petrol and thirty rupees a litre on diesel. PIB figures of 27 March 2026 reported under-recoveries at the refinery gate of twenty-six rupees a litre on petrol and eighty-one rupees and ninety paise a litre on diesel. The 27 March SAED cut transferred ten rupees of the petrol gap and ten rupees of the diesel gap from the consumer to the exchequer.

An export levy was imposed simultaneously with the 27 March 2026 cut, at twenty-one rupees and fifty paise a litre on diesel and twenty-nine rupees and fifty paise a litre on ATF, to keep Indian-produced fuel in the Indian market and prevent the domestic supply from being pulled out by international price arbitrage. The export levy contributed to the SAED cut being a net protection of the Indian consumer rather than a revenue giveaway to refiners.

The retail price of petrol and diesel in Delhi has moved by under one per cent in either direction over the four years from February 2022 to February 2026, against a Brent benchmark that has moved sharply in both directions across the same period. The OMC revision of 15 May 2026, ninety-one paise on each fuel, is the first material upward movement of the retail price in nearly four years.

4. International comparison: 23 February to 15 May 2026

Through the seventy-six days from the closure of the Strait of Hormuz on 28 February 2026 to the OMC revision of 15 May, India held petrol and diesel prices essentially unchanged while the rest of the world raised prices by ten, twenty, fifty, and in some cases ninety per cent. The OMC revision today, of ninety-one paise per litre on both fuels, takes the headline movement on the Indian retail price to just over four per cent. The table below sets out the country-by-country change in local currency at the pump.

Source: GlobalPetrolPrices.com weekly retail data, country-level changes from 23 February 2026 to 11 May 2026. India entry updated to reflect the OMC revision of 15 May 2026.

The Indian revision of ninety-one paise a litre, equivalent to just over four per cent on a base of about ninety-five rupees, is the smallest material upward movement of any major economy outside the directly subsidising Gulf producers. The contrast is the context.

5. State-level VAT: where the pump price actually diverges

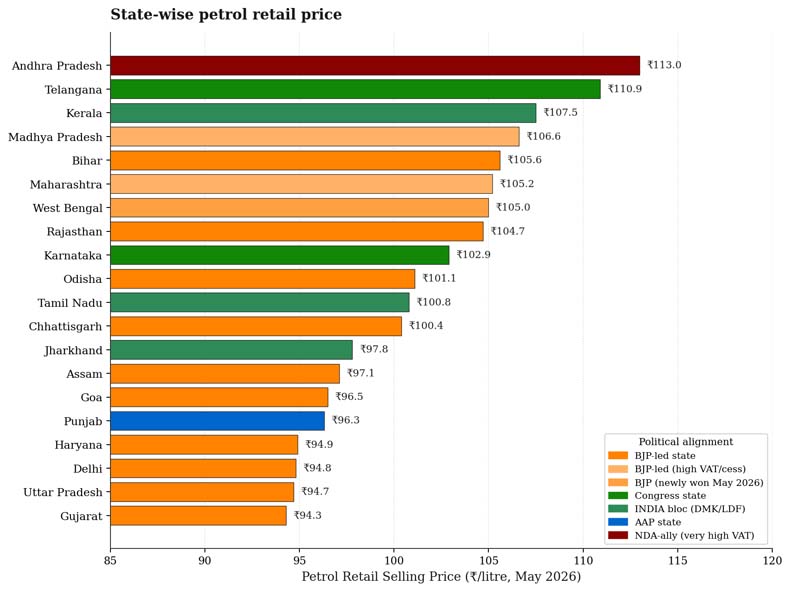

The central excise component of the petrol and diesel price is the same in every state of the Union. The pump price diverges because of the value added tax that each state government separately levies. The states with the highest VAT impose effective rates of thirty per cent and more, often layered with per-litre additions and infrastructure cesses. The states with the lowest impose rates closer to twenty per cent, no per-litre addition, and no further cess. The geographical map of the divergence is, with a few exceptions, the political map of the divergence.

Petrol retail selling price by state, mid-May 2026. States with the highest pump prices are concentrated in the Congress-ruled and INDIA-bloc south (Telangana, Kerala, Karnataka, Tamil Nadu) and in a single NDA-allied outlier (Andhra Pradesh, where the TDP state government levies an exceptionally high VAT plus per-litre addition). States with the lowest pump prices are concentrated in the BJP-ruled north and west: Gujarat, Uttar Pradesh, Delhi, Haryana, Goa, Assam. Maharashtra and Madhya Pradesh are BJP-led but carry a higher VAT or recent cess, and read accordingly in the upper-middle band. Source: MoPNG Lok Sabha replies and city-level RSP data, updated to May 2026.

Three states have petrol above one hundred and seven rupees a litre: Andhra Pradesh, Telangana, and Kerala. Telangana and Kerala are governed by parties of the INDIA bloc. The same three states levy the highest VAT rates in the country: Andhra Pradesh charges 31 per cent VAT plus four rupees a litre plus a road development cess, taking the effective rate close to thirty-five per cent. Telangana takes petrol to over one hundred and ten rupees. Kerala adds a social security cess on top of its base VAT.

Six states have petrol at or below ninety-seven rupees a litre: Gujarat, Uttar Pradesh, Delhi, Haryana, Goa, and Assam. All six are governed by the BJP. The same opposition leaderships that ask the central government to cut excise duty for the relief of the consumer have at no point cut the value added tax their own state governments levy on the same litre of fuel. When the central excise duty was cut on 27 March 2026 by ten rupees a litre on petrol and diesel, the BJP-ruled states passed the full cut through to the pump. The Congress-ruled and INDIA-bloc states did not separately reduce VAT, which means the percentage-based VAT captured a smaller share of the now-lower base, but the consumer in those states still pays more than the consumer in a BJP-ruled state directly because of state taxation.

The framing that the central government overtaxes fuel collapses against the state-level data. The states that tax fuel hardest are not the centre. They are the political opponents of the centre.

Summary

Through four years that included the Russia–Ukraine war and the closure of the Strait of Hormuz, the Government of India cut the central excise on petrol and diesel four times, absorbed approximately thirty thousand crore rupees of revenue at the exchequer in the most recent cut alone, and redeemed over one lakh thirty thousand crore rupees of UPA-era oil bonds, principal alone.

India is the only major economy in the world to have cut retail fuel prices through the Russia–Ukraine window. India is the only major economy in the world to have held retail fuel prices essentially unchanged through the Hormuz disruption.

The OMC revision of ninety-one paise on 15 May 2026, after seventy-six days of complete absorption, is the smallest material upward movement of any major economy outside the directly subsidising Gulf producers. The states that tax fuel most heavily are governed by the political opposition. The architecture of consumer protection, the redemption of past liabilities, and the absorption of present losses are the work of the present government.