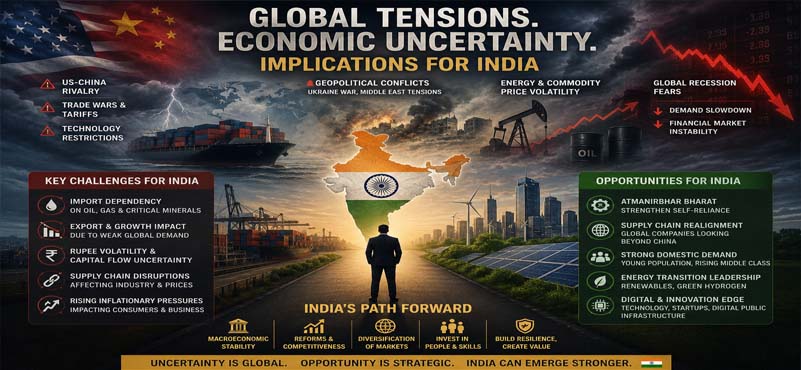

India’s external-sector position cannot be understood in isolation, in silo, from the profound changes occurring in the global economy. The post-Cold War era of increasing globalisation, relatively free capital mobility and stable trade relationships is gradually giving way to an environment characterised by geopolitical rivalry, strategic protectionism and economic fragmentation.

The wars in Ukraine and West Asia, disruptions in the Red Sea shipping corridor, sanctions regimes, technological restrictions and growing US-China rivalry have heightened uncertainty in global trade and investment flows. The IMF, World Bank and WTO have repeatedly warned that geoeconomic fragmentation could reduce global growth and weaken trade efficiency.

For India, these developments create both risks and opportunities. Supply-chain diversification away from China offers India an opportunity to attract investment in electronics, semiconductors, renewable energy equipment and advanced manufacturing. However, heightened geopolitical tensions can increase commodity-price volatility, particularly for crude oil and natural gas, thereby worsening India’s trade balance. External vulnerability today is, therefore, shaped as much by geopolitics as by economics.

Domestic Growth

The macroeconomic overlay is under strain from rising crude oil prices and a growing import bill, which are squeezing both the fiscal and current account deficits. These challenges are compounded by persistent inflationary pressures, capital outflows, declines in the Nifty and Sensex, rupee depreciation, slowing private consumption, widening income and wealth inequality, agricultural distress, infrastructure and urban bottlenecks, and deficiencies in human capital development. However, the external sector assumes significance due to ongoing instability in West Asia, rising geoeconomic fragmentation, persistent oil price volatility, tightening global financial conditions, and repeated safe-haven capital flows into advanced economies.

For a large and globally integrated economy such as India, external-sector resilience is no longer merely a matter of trade performance; it is increasingly linked to capital flows, currency stability, reserve adequacy, external debt sustainability, and investor confidence. There’s a battle inside and a war outside. Assessing India’s external vulnerability requires a holistic view of interconnected factors rather than a narrow focus on any single indicator. For, as Sahir Ludhianvi cogently argued,

“नहीं है नाउम्मीद इक़बाल अपनी किश्त–ए–वीराँ से,

बड़ी ज़रख़ेज़ है मिट्टी, ज़रा नम हो तो ये साक़ी।”

Meaning: Even a barren field can bloom again if it receives a little nourishment.

Oil Dependence: A Persistent Structural Weakness

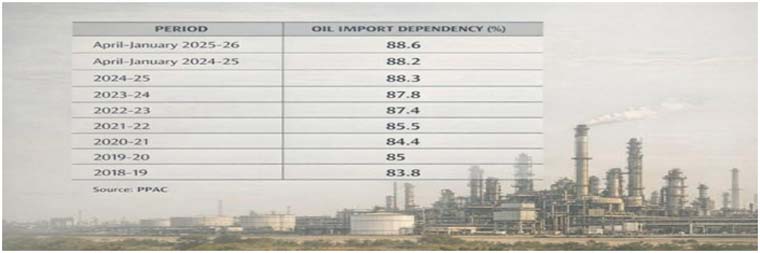

Despite significant progress in renewable energy, India remains heavily dependent on imported crude oil. India imports approximately 85% of its crude oil requirements. Consequently, fluctuations in global oil prices disproportionately influence the current account deficit, inflation, fiscal balances, and exchange-rate stability. Historically, every major episode of external-sector stress in India has coincided with elevated oil prices, e.g., the 1973 oil shock, the 1979 oil shock, the 1990 Gulf War, the 2008 commodity boom, the 2022 Russia-Ukraine conflict, and recent West Asian tensions.

A sustained increase of US$10 per barrel in crude prices can significantly increase India’s import bill and widen the current account deficit. The challenge is compounded because oil imports are denominated largely in US dollars. Higher oil prices, therefore, simultaneously increase import expenditure and foreign-exchange demand. Reducing energy dependence is an important long-term strategy for strengthening external resilience. Accelerated deployment of solar and wind energy, expansion of electric mobility, green hydrogen initiatives and improvements in energy efficiency can gradually reduce exposure to imported fossil fuels.

Volatile Capital Inflows: Basic Risk

India has traditionally financed its current account deficit (CAD) through foreign direct investment (FDI), portfolio investment, external commercial borrowings (ECBs), and remittance inflows. While this financing model has generally worked well, it also leaves the economy exposed to shifts in global risk appetite and international liquidity conditions. The mix of capital inflows is particularly important. FDI is long-term, productivity-enhancing, and relatively stable even during periods of global turbulence. Portfolio investments, by contrast, are highly sensitive to interest-rate differentials, geopolitical uncertainty, exchange-rate expectations, and changes in investor sentiment. Consequently, sudden reversals in portfolio flows exacerbate pressure on the rupee and foreign exchange reserves, despite sound underlying economic fundamentals.

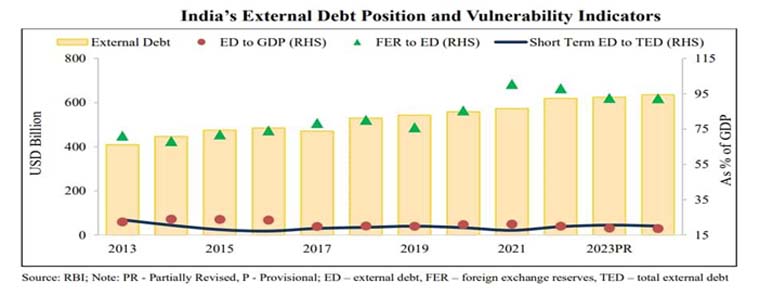

India’s relatively comfortable external debt indicators provide an important cushion. India’s projected 55.6% central government debt-to-GDP ratio in FY27 remains moderate by international standards; the share of short-term debt in total external debt at 18.4% at end-September 2025 is manageable; and debt-service indicators (external debt service ratio at 6.0%, total external debt at 19.2% of GDP, foreign exchange reserves cover 93.8% of India’s total external debt) remain broadly benign. The sustainability of external financing, however, depends not only on the quantity but also on the quality and stability of capital inflows. Therefore, the central policy challenge is not a lack of foreign capital but ensuring that a larger share of incoming capital is stable, long-term, and less prone to sudden reversals.

India’s Need for Foreign Capital and Its Capacity to Attract It

A distinction between the demand for foreign capital and the economy’s attractiveness as a global investment destination is necessary. India continues to attract substantial FDI across manufacturing, digital services, infrastructure, renewable energy, financial services, and emerging technology sectors. India’s large domestic market, improving digital infrastructure, expanding middle class, and ongoing structural reforms support its investment appeal.

Moreover, India’s external vulnerability indicators do not presage a financing crisis. A robust services trade surplus, particularly in information technology (IT) and business services, together with consistently strong remittance inflows from overseas Indians, makes foreign exchange earnings durable. The challenge lies primarily in volatile financial flows rather than in any structural inability to attract capital. Consequently, policy efforts must focus on improving investment certainty, strengthening institutions, reducing regulatory frictions, and expanding investment opportunities rather than responding in a crisis-management mode.

Services Exports: India’s Strong External Buffer

Services exports represent India’s greatest structural strength. Unlike commodity exports, services exports rely primarily on human capital, technological capability and knowledge-intensive activities. India’s information technology industry has evolved into a globally competitive sector generating substantial foreign-exchange earnings.

Services exports now extend beyond traditional IT outsourcing and increasingly include business-process management, financial services, engineering design, research and development, legal services, digital platforms, and artificial intelligence and analytics. The significance of services exports transcends their size. They tend to be less volatile than capital flows and less vulnerable to commodity-price fluctuations. This provides a stable source of foreign exchange that partially offsets India’s chronic merchandise trade deficit. The services sector effectively functions as India’s invisible export engine.

Tax Incentives and Market Deepening: A Strategic, Not Defensive, Approach

Global investors increasingly prefer economies with stable and predictable policy environments in all their forms and manifestations. In India, concerns regarding retrospective taxation, regulatory unpredictability and compliance burdens have affected investor sentiment. Recent measures by the RBI and the Government of India aimed at enhancing the attractiveness of Indian financial markets, including tax concessions and capital-gains relief on selected government securities, should be viewed within the broader framework of capital-market deepening, easing pressure on the rupee and narrowing part of the balance of payments gap.

The RBI’s plan comprises

- FCNR(B) deposits of three to five years are to be exempt from Cash Reserve Ratio (CRR), Statutory Liquidity Ratio (SLR), lowering the cost of mobilising such funds.

- For external commercial borrowings (ECBs), RBI has set a swap cost of 1.5 %, making overseas loans attractive for top-rated PSUs compared with domestic funding

- FCNR(B) swap window will remain open until October 16, 2026, for deposits mobilised up to September 30.

- The ECB and OFCB swap facility will run until January 15, 2027, for drawdowns up to December 31, 2026.

Such contextually significant measures broaden investor base, improve market liquidity, reduce financing costs, and integrate domestic financial markets more closely with global capital markets. They are consistent with practices followed by many emerging and advanced economies seeking to attract long-term institutional investors. The rationale transcends inflows. A deeper and more diversified investor base reduces concentration risks and enhances market resilience during volatile periods. While greater foreign participation inevitably causes susceptibility to global market fluctuations, the overall objective is to improve the efficiency and depth of domestic capital markets. These measures, therefore, represent a strategic effort to strengthen India’s long-term financial architecture rather than a response to immediate external stress.

Capital Account vs. Current Account: Which Presents the Greater Risk?

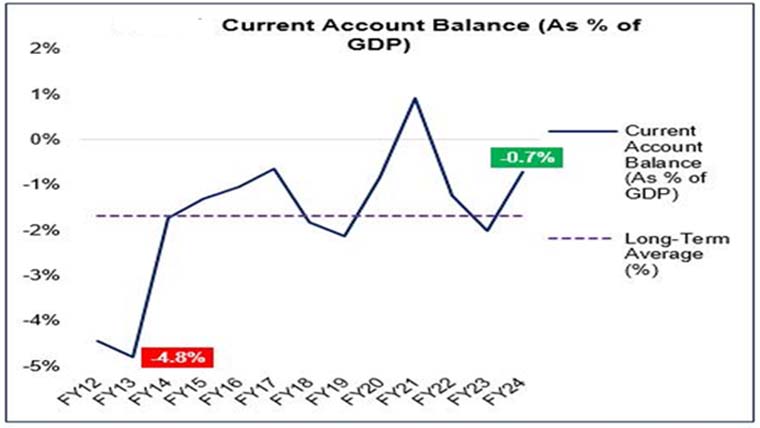

Conventional discussions of external vulnerability often focus on the current account deficit. However, in contemporary emerging-market economies (EMEs), instability frequently originates from the capital account. India’s current account dynamics remain relatively manageable. The merchandise trade deficit is partially offset by a substantial services surplus and a large remittance inflow. While fluctuations in global commodity prices, especially crude oil, can widen the CAD, these pressures have generally remained manageable.

The capital account is more complex. Portfolio flows can reverse rapidly in response to external developments unrelated to domestic fundamentals. Changes in US monetary policy, geopolitical conflicts, financial-market stress, or global risk aversion can trigger large-scale capital movements.

International cross-country experience demonstrates that many external crises emerge not because of excessive current account deficits alone, but also because of sudden stops or reversals in capital flows. Consequently, close monitoring of the composition, maturity profile, and stability of capital inflows is essential. From an external-sector risk perspective, instability in capital flows warrants greater attention than the current account deficit.

Remittances: The Silent Stabiliser

India has consistently ranked among the world’s largest recipients of remittances. The Indian diaspora is spread across North America, Europe, the Gulf region, Australia and Southeast Asia. Unlike portfolio flows, remittances are remarkably resilient during periods of financial turbulence and provide a reliable source of foreign exchange. Remittance inflow at $110.47 billion in FY 26 is a natural shock absorber and a key differentiator.

Reserve Adequacy: Are India’s Reserves Sufficient?

Foreign-exchange reserves remain India’s most visible line of defence against external shocks. Reserve adequacy can be evaluated through several metrics:

Import Cover

India’s reserves currently cover roughly eleven months of imports. The traditional benchmark is three months. India, therefore, comfortably exceeds conventional standards.

External Debt Coverage

A key indicator is the ratio of reserves to total external debt. High coverage implies greater ability to meet external obligations during periods of market stress.

Guidotti-Greenspan Rule

This rule suggests that countries should maintain reserves sufficient to cover all short-term external debt falling due within one year. India currently remains well-positioned under this benchmark. Nevertheless, reserve adequacy should not create complacency. Reserve accumulation is necessary but not sufficient. The best protection against external crises remains sustained foreign-exchange earning capacity.

If Capital Inflows Weaken, Where Would Pressure Manifest First?

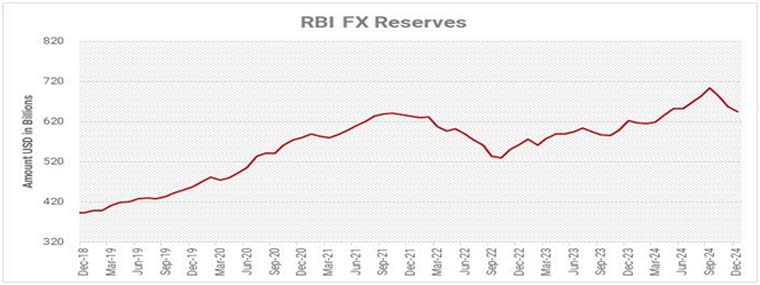

Should capital inflows weaken significantly, the pressure would likely emerge first in the foreign exchange market. Reduced capital inflows lower the supply of foreign currency, exerting downward pressure on the rupee. While moderate depreciation can help improve export competitiveness, sharp or disorderly movements can increase imported inflation, raise external financing costs, and affect investor confidence. Subsequently, foreign exchange reserves would be hit, requiring the RBI’s intervention to smooth excessive currency volatility, drawing upon reserve buffers. Although India’s forex reserves at $682.32 billion as on May 29, 2026 (constituting about eleven months of imports) are substantial by historical standards, prolonged intervention could gradually erode these cushions, leading to a tightening of domestic liquidity conditions as foreign capital availability declines. Higher bond yields, increased financing costs, and tighter credit conditions may then hamper investment and growth prospects.

Therefore, the stress would transmit sequentially: decelerating capital flows would lead to rupee depreciation, prompting reserve drawdowns. That, in turn, would tighten liquidity, raise borrowing costs, and moderate growth. This vicious cycle would cause extensive concern, if not consternation, wouldn’t it? India’s sizeable reserve stockpile significantly slows this transmission mechanism, but exchange-rate volatility remains the most immediate manifestation of external stress.

India’s Greatest Buffer and Key Vulnerability

Unlike portfolio flows, services exports are driven by long-term competitiveness, global outsourcing trends, technological capabilities, and accumulated human capital. Remittance inflows constitute a second important stabilising force. Foreign exchange reserves represent the third and most visible line of defence. They provide the capacity to smooth exchange-rate volatility, meet external payment obligations, and reassure financial markets regarding India’s ability to withstand shocks.

Paradoxically, however, reserves are also most exposed during severe global financial turbulence. Their effectiveness depends on the scale and duration of external pressures. Reserves can absorb shocks, but they cannot permanently offset persistent capital outflows. Consequently, India must strengthen its structural foreign-exchange earning capacity through services exports, remittances, export diversification, and sustained productivity growth rather than rely solely on reserve accumulation.

Key Indicators of External Financing Stress- The Form and Substance

Policymakers should track a broad set of indicators, not a single metric. Key warning signs include portfolio outflows and sustained withdrawals by foreign investors; rapid rupee depreciation and volatility; reserve depletion from prolonged intervention; widening current account deficits, especially due to oil imports; slowing FDI inflows; rising external debt, particularly short-term debt relative to reserves; increasing debt-service burdens; weakening import-cover ratios; higher sovereign and corporate external borrowing costs; and persistent gaps between domestic and global interest rates that may trigger capital outflows. While no single threshold automatically signals crisis conditions, policymakers should be increasingly concerned if rapid currency depreciation, sustained reserve losses, widening CADs, and significant portfolio outflows occur simultaneously. External-sector crises rarely emerge suddenly; a gradual deterioration across multiple indicators usually precedes them, as Nobel Laureate Ernest Hemingway wrote (“Two ways. Gradually, then suddenly”) in his novel The Sun Also Rises, a point that resonates deeply with the dynamics of global change.

Manufacturing and Export Competitiveness

An enduring challenge is the relatively limited role of manufacturing exports compared with East Asian economies. China, Vietnam, South Korea and Taiwan achieved rapid export growth through integration into global manufacturing value chains.

India’s exports at $ 863.11 billion in FY 26 remains more concentrated. Key constraints include logistics costs, land acquisition challenges, regulatory complexity, skill gaps, and infrastructure bottlenecks. The Production Linked Incentive (PLI) schemes are important in improving manufacturing competitiveness. However, long-term success will require deeper reforms in labour markets, logistics, education and infrastructure. A stronger manufacturing export base would diversify foreign-exchange earnings and reduce external vulnerability.

Capital Flows and the New Financial Cycle: An Indian Perspective

I argued in my well-received two-volume book (co-authored with K.R. Gupta) entitled Global Economic Meltdown (published by Atlantic Publishers, New Delhi, 2012) that the nature of global finance has changed significantly over the decades. Financial markets have become increasingly integrated, and capital flows across countries are now influenced not only by domestic economic conditions but also by global liquidity, investor sentiment, and the monetary policy decisions of major central banks, particularly the US Federal Reserve. As a result, economists increasingly refer to a “global financial cycle”, a phenomenon in which cross-border capital flows, asset prices, exchange rates, and financial conditions move together across countries, irrespective of their domestic economic fundamentals.

Research by economist Hélène Rey shows that the traditional concept of an independent monetary policy under a floating exchange rate has become more constrained because global capital markets are heavily influenced by the monetary conditions of the US. When US interest rates remain low and global liquidity is abundant, investors search for higher returns in emerging markets such as India, leading to strong capital inflows. Conversely, when the Federal Reserve tightens monetary policy and raises interest rates, capital often flows back to advanced economies, causing pressure on emerging-market currencies, bond markets, and external balances.

India’s experience over the last three decades illustrates the growing influence of this global financial cycle. During periods of global liquidity expansion, India has benefited from substantial foreign capital inflows through foreign portfolio investment (FPI), FDI, external commercial borrowings (ECBs), and banking flows. These inflows have helped finance current account deficits, strengthen foreign exchange reserves, support corporate investment, and deepen domestic financial markets. However, they have also increased India’s exposure to sudden shifts in global risk appetite.

The global financial crisis (2008-09) starkly highlighted this vulnerability. Although India’s banking system remained relatively insulated from toxic financial assets, the sudden withdrawal of foreign portfolio capital led to a sharp decline in equity markets and significant pressure on the rupee. Net portfolio outflows accelerated as global investors sought safety in US Treasury securities and other low-risk assets. The crisis revealed that even economies with sound domestic fundamentals could experience financial stress when global risk sentiment deteriorated.

A more striking example emerged during the 2013 “Taper Tantrum.” In May 2013, the Federal Reserve signalled that it would begin reducing its quantitative easing programme. The announcement triggered a wave of capital outflows from emerging markets. India was grouped among the so-called “Fragile Five” economies because of its relatively large current account deficit and dependence on foreign capital. Between May and August 2013, the rupee depreciated sharply, touching record lows, while bond yields rose and equity markets were significantly volatile. The episode underscored how quickly external financing conditions can change when global investors reassess risk.

The most recent example occurred during the post-pandemic monetary tightening cycle of 2022-24. Following the surge in global inflation after COVID-19 and the Russia-Ukraine conflict, the Federal Reserve implemented one of the fastest interest-rate hiking cycles in decades. Higher US yields attracted capital back to American financial markets, leading to substantial portfolio outflows from many emerging economies. India also experienced episodes of FPI withdrawals, exchange-rate pressures, and heightened market volatility. Although India’s macroeconomic fundamentals were stronger than during previous episodes, the experience brought to the fore the continuing influence of global financial conditions on domestic financial markets.

The composition of capital flows matters because not all foreign capital is equally stable. FDI is generally the most dependable source of external financing, as it is tied to long-term productive investment. However, FDI itself varies in quality. Real FDI (RFDI) comes from multinational firms that bring technology, brands, and production capabilities. Financial investors, viz., private equity, venture capital, and asset management funds, primarily seek capital gains and eventual exits. Diaspora investments and special purpose vehicles (SPVs) channel overseas capital through offshore centres and may sometimes involve the round-tripping of domestic funds.

Portfolio flows into equity and debt markets, by contrast, can be highly volatile and sensitive to changes in global interest rates, geopolitical risks, and investor sentiment. Consequently, a country may appear externally comfortable during periods of strong inflows but face sudden financing pressures when global conditions change.

India’s growing integration with global financial markets has increased both opportunities and vulnerabilities. Greater access to foreign capital has supported infrastructure development, technological upgrading, startup financing, and corporate expansion. India has also benefited from inclusion in major global bond and equity indices, which have broadened the investor base and improved market liquidity. Yet greater integration also means that external shocks can be transmitted more rapidly into domestic financial markets.

A key concern is the possibility of a “sudden stop” in capital inflows. Such episodes occur when foreign investors abruptly reduce their exposure to emerging markets in response to global shocks rather than country-specific weaknesses. A sudden stop can trigger currency depreciation, higher borrowing costs, declining asset prices, and pressure on foreign exchange reserves. Countries with large external financing requirements are particularly vulnerable. Although India’s external position is stronger than in the past, policymakers must monitor these risks.

To manage the challenges posed by the global financial cycle, India has adopted a multi-layered strategy. First, the country has accumulated substantial foreign exchange reserves, which serve as a buffer against external shocks and help maintain confidence during periods of capital outflows. India’s reserves have generally remained among the largest in the world, providing the RBI with significant intervention capacity.

Second, the RBI has developed considerable credibility in conducting monetary policy and managing exchange-rate volatility. While the rupee is allowed to adjust to market conditions, excessive volatility is often moderated through foreign exchange market interventions. This approach helps reduce the risk of destabilising currency movements without attempting to maintain a fixed exchange rate.

Third, maintaining fiscal discipline remains essential. Countries with large fiscal deficits are often perceived as riskier during periods of global financial stress because investors worry about macroeconomic stability. Sustainable public finances strengthen investor confidence and reduce vulnerability to external shocks.

Fourth, India has sought to deepen domestic financial markets. A broader and more diversified domestic investor base, including banks, insurance companies, pension funds, mutual funds, and retail investors, can reduce dependence on foreign capital. The increasing participation of domestic institutional investors in Indian equity and bond markets has helped cushion the impact of foreign portfolio outflows in recent years.

Fifth, policymakers are increasingly emphasising the quality rather than merely the quantity of capital inflows. Encouraging stable FDI, long-term infrastructure financing, sovereign wealth fund participation, and strategic investments can reduce reliance on volatile portfolio flows. Improved ease of doing business, strengthened regulatory frameworks, and enhanced investor protection are important.

Looking ahead, India’s external sector will continue to operate in an environment shaped by global financial cycles, geopolitical uncertainty, technological change, and evolving patterns of international capital movement. The rise of geoeconomic fragmentation, growing public debt in advanced economies, shifts in global supply chains, and increasing climate-related financial risks could further complicate the dynamics of capital flow. Consequently, external sector management can no longer focus solely on trade balances or current account deficits; it must also account for the behaviour of global financial markets and cross-border capital flows.

Climate Change and External Vulnerability

An emerging dimension of external vulnerability is climate risk. Extreme weather events can affect agricultural exports, food inflation, rural incomes, energy demand, and insurance costs. Climate-related trade measures, including carbon border adjustment mechanisms in advanced economies, may also affect India’s export competitiveness. External-sector strategy increasingly needs to incorporate sustainability considerations. Green exports, renewable-energy manufacturing and climate-resilient infrastructure are becoming economic imperatives rather than environmental luxuries.

Echoes of the 1991 Balance-of-Payments Crisis?

Comparing India’s current external position with the 1991 balance-of-payments crisis is odious. In 1991, India faced a genuine external financing emergency characterised by critically low foreign exchange reserves, weak export competitiveness, large fiscal imbalances, limited access to international capital markets, and a narrow foreign-exchange-earning base. Reserves had fallen to levels sufficient for only a few weeks of imports, forcing India to seek emergency external assistance and pledge gold as collateral. India is, however, not immune to external shocks.

Rising oil prices, geopolitical tensions, and sudden shifts in global capital flows continue to pose risks. However, the major vulnerability is not external insolvency but financial volatility. Episodes such as the global financial crisis of 2008, the taper tantrum of 2013, and the post-pandemic tightening cycle revealed that even economies with strong fundamentals can experience capital outflows, currency pressure, and financial-market turbulence when global conditions deteriorate.

The policy challenge, therefore, is not crisis management but risk management, necessitating prudent macroeconomic policies, adequate reserve buffers, diversified export earnings, stable long-term capital inflows, deeper domestic financial markets, and reduced dependence on imported energy. Sustained institutional credibility and investor confidence are also important. India possesses substantial foreign exchange reserves, a diversified export basket, a globally competitive services sector, strong remittance inflows, deeper financial markets, a flexible exchange-rate regime, and significantly stronger macroeconomic institutions. External debt remains manageable, while reserve adequacy indicators are far stronger than those prevailing in the early 1990s.

The Road Ahead

India’s external sector today is fundamentally different from the fragile economy of 1991. Large foreign-exchange reserves, a globally competitive services sector, strong remittance inflows, a relatively manageable external debt profile, and more sophisticated policy institutions provide substantial protection against external shocks. Yet resilience should not be confused with invulnerability. The principal risks arise from volatile capital flows, energy dependence, geopolitical instability, and an increasingly fragmented global economy. However, external vulnerability should not be assessed through isolated prisms or alarmist comparisons with past crises. The challenge is not merely to accumulate reserves but to strengthen the underlying capacity to earn foreign exchange through diversified exports, technological upgrading, manufacturing competitiveness and sustained productivity growth. As Faiz Ahmed Faiz wrote powerfully,

“दिल न–उम्मीद तो नहीं, नाकाम ही तो है

लम्बी है ग़म की शाम, मगर शाम ही तो है।”

Meaning: The heart has not lost hope; it has merely faced setbacks. The evening of sorrow may be long, but it is still only an evening; it will pass. This too shall pass!

I have long held, perhaps not unjustifiably, that India’s external sector remains supported by a strong services trade surplus, steady remittance inflows, a manageable external debt profile, and substantial foreign exchange reserves. The greater vulnerability lies in volatile capital flows, particularly foreign portfolio investment, which are highly sensitive to global financial conditions. Policy should therefore focus on improving the quality and stability of external financing, deepening domestic financial markets, enhancing export competitiveness, and maintaining adequate reserve buffers. Strengthening trade integration with ASEAN and the European Union can boost exports and facilitate greater participation in global value chains.

Production-linked incentive schemes should be expanded to labour-intensive sectors to support manufacturing growth and employment generation. Reducing dependence on imported energy is equally critical for external stability. Bringing petroleum products and electricity under the GST framework could improve efficiency and lower costs. India must also deepen its corporate bond market and strengthen domestic sources of long-term capital to reduce reliance on volatile portfolio flows. These reforms would cumulatively enhance external sector resilience, improve the economy’s capacity to absorb global shocks, and ensure greater stability amid future economic and geopolitical uncertainties.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.