This presentation was delivered at the Gokhale Institute, Pune, as Kale Memorial Lecture, last month; Dr Shaktikanta Das is presently the principal private secretary to the prime minister of India.

I am delighted to be here at the Gokhale Institute of Politics and Economics (GIPE), Pune to deliver the 85th Kale Memorial Lecture. It gives me a great sense of humility to know that stalwarts like Dr. B. R. Ambedkar, Shri. P. C.Mahalanobis, Shri. V.K.R.V. Rao, Shri C Rangarajan, Shri A.P.J. Abdul Kalam and others had delivered this lecture in the previous years.

Like the mammoth Banyan tree in the historical campus of GIPE, this tradition of Kale Memorial Lecture has prospered through accretion of wisdom of ages and I feel absolutely honoured to be the part of the same. I sincerely thank the Gokhale Institute for having given me this opportunity.

Like the mammoth Banyan tree in the historical campus of GIPE, this tradition of Kale Memorial Lecture has prospered through accretion of wisdom of ages and I feel absolutely honoured to be the part of the same. I sincerely thank the Gokhale Institute for having given me this opportunity.

On this occasion, I wish to share some of my thoughts on the Indian Economy in a Changing Global Order. The global economy is going through a phase of unprecedented uncertainty and fundamental reset. A rules-based trading framework that promoted globalisation and free trade for over eight decades is under challenge. Established rules are being increasingly questioned while new norms are yet to be firmly established. The COVID-19 pandemic and the Ukraine-Russia conflict have accelerated the move toward self-reliance. Vulnerabilities in global supply chains have led many nations to rethink their external dependencies and give higher importance to supply chain resilience over cost efficiency. Strategic autonomy is now a top priority. This transformation is also evident in the growing influence of regional trade agreements (RTAs), which reflect a shift towards more fragmented yet practical trade alliances. The year 2025, in nutshell, is a pivotal year in terms of global economic trajectory.

In this uncertain global environment, India continues to demonstrate remarkable dynamism and resilience. Guided by a decade of structural reforms and strategic global positioning under the vision of “Atmanirbhar Bharat”, the nation has successfully weathered multiple global headwinds. India’s robust domestic demand, together with prudent macroeconomic and financial sector policies, has enabled the country to withstand many external shocks. India is now poised to contribute about one-fifth of the world’s GDP growth.

In this uncertain global environment, India continues to demonstrate remarkable dynamism and resilience. Guided by a decade of structural reforms and strategic global positioning under the vision of “Atmanirbhar Bharat”, the nation has successfully weathered multiple global headwinds. India’s robust domestic demand, together with prudent macroeconomic and financial sector policies, has enabled the country to withstand many external shocks. India is now poised to contribute about one-fifth of the world’s GDP growth.

India has also been actively reshaping its trade engagements to align with the changing global order. India is a signatory to 14 free trade agreements (FTAs) and six preferential trade agreements (PTAs), with the UK, Australia and the UAE being the recent additions among FTAs. Additionally, members of European Free Trade Association – Iceland, Liechtenstein, Norway, Switzerland and India have signed a comprehensive Trade and Economic Partnership Agreement in March 2024. At present, India is in free trade agreement negotiations with the US, the EU, Peru, Oman, New Zealand, among several others. The underlying priority of our trade negotiations is to secure fair and balanced agreements in the best interest of our nation and the people.

Amidst such a changing global order, it would be important to focus on the robust fundamentals that impart strength to the Indian economy and the structural reforms that have strengthened these fundamentals. These factors have enabled India to navigate through the tumultuous world order.

Amidst such a changing global order, it would be important to focus on the robust fundamentals that impart strength to the Indian economy and the structural reforms that have strengthened these fundamentals. These factors have enabled India to navigate through the tumultuous world order.

Strength of India’s Macroeconomic Fundamentals

- Economic Growth

India continues to record impressive growth, as several favourable factors, such as a younger demography and greater reliance on domestic demand, provide the strength to withstand the negative spillovers from global turbulence. India’s average economic growth during 2014-15 to 2024-25 was 7.1 per cent (excluding the Covid-19 years of 2020-21 and 2021-22). In the last three years (2022-23 to 2024-25), GDP growth averaged 7.8 per cent. Further, the provisional estimates (PE) of national income released by the National Statistical Office (NSO) has placed India’s real GDP growth at 6.5 per cent for 2024-25. The growth for 2025-26 is expected to be 6.8 per cent as per the latest forecast given by the Reserve Bank of India.

India is fast emerging as an economic powerhouse and is projected to become the fourth-largest global economy in 2025 and the third-largest in 2028, driven by domestic reforms and a strong global positioning under the vision of Atmanirbhar Bharat.

At the broad sectoral level, India’s manufacturing sector has expanded at an average pace of 5.9 per cent over the past decade. Recognising the sector’s critical role in generating employment and in unlocking the nation’s export potential, the government has introduced a series of reforms to revitalise the manufacturing sector.

At the broad sectoral level, India’s manufacturing sector has expanded at an average pace of 5.9 per cent over the past decade. Recognising the sector’s critical role in generating employment and in unlocking the nation’s export potential, the government has introduced a series of reforms to revitalise the manufacturing sector.

These measures include the rationalisation of corporate tax rates, the Make in India initiative, the Production Linked Incentive (PLI) scheme, the Start-up India programme, and comprehensive Ease of Doing Business reforms. All these measures are aimed at strengthening competitiveness and driving industrial growth.

Measures like adoption of technology for delivery of services, FDI reforms, opening up sectors like space and mining to private sector participation and consistent emphasis on reduction of compliance burden have led to increase in capacity and efficiency of the economy.

The higher focus on government capex, infra initiatives like the recently announced 12 industrial cities and 100 industrial parks near urban centres are increasing the efficiency of logistics and costs for the manufacturing sector.

Today there is vibrancy almost in every aspect of the manufacturing sector. Let me list out a few-

The PLI scheme has achieved remarkable milestones in terms of investment, production and job creation. Across 14 sectors, it has facilitated investment of ₹1.76 lakh crore, incremental production/sales of over ₹16.50 lakh crore and employment generation of over 12 lakhs.

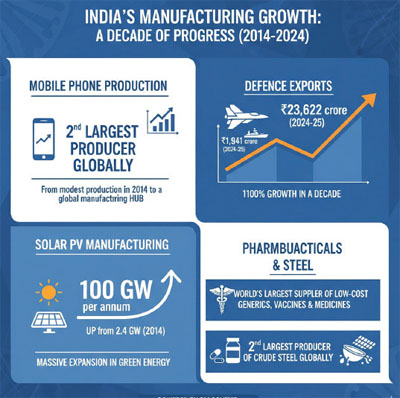

Today, India has emerged as the second largest producer of crude steel and mobile phones in the world.

Today, India has emerged as the second largest producer of crude steel and mobile phones in the world.

India is the world’s largest supplier of low-cost generics, vaccines and affordable medicines.

India’s solar PV module manufacturing has increased dramatically from 2.4 GW per annum in 2014 to 100 GW per annum.

India’s defence exports have surged from ₹1,941 crore in FY 2014-15 to ₹23,622 crore in FY 2024-25, reflecting a remarkable increase in export value.

In the next 3 to 4 years, industrial growth is expected to be driven by a combination of traditional and emerging sectors. Traditional manufacturing industries such as electronics, auto components, chemicals and pharmaceuticals are projected to grow steadily. At the same time, new-age and high-growth sectors are also expected to expand rapidly, benefiting from supply chain diversification and strategic policy support. Indian manufacturers are increasingly adopting Industry 4.0 and 5.0 technologies such as robotics, AI, Internet of things (IoT), smart factory systems and digital twins to boost productivity and efficiency. With a sharp focus on sunrise industries like semiconductors, EVs, renewable energy, biotechnology, the space economy and green hydrogen, India is well- positioned to capture significant long-term gains from this industrial transformation.

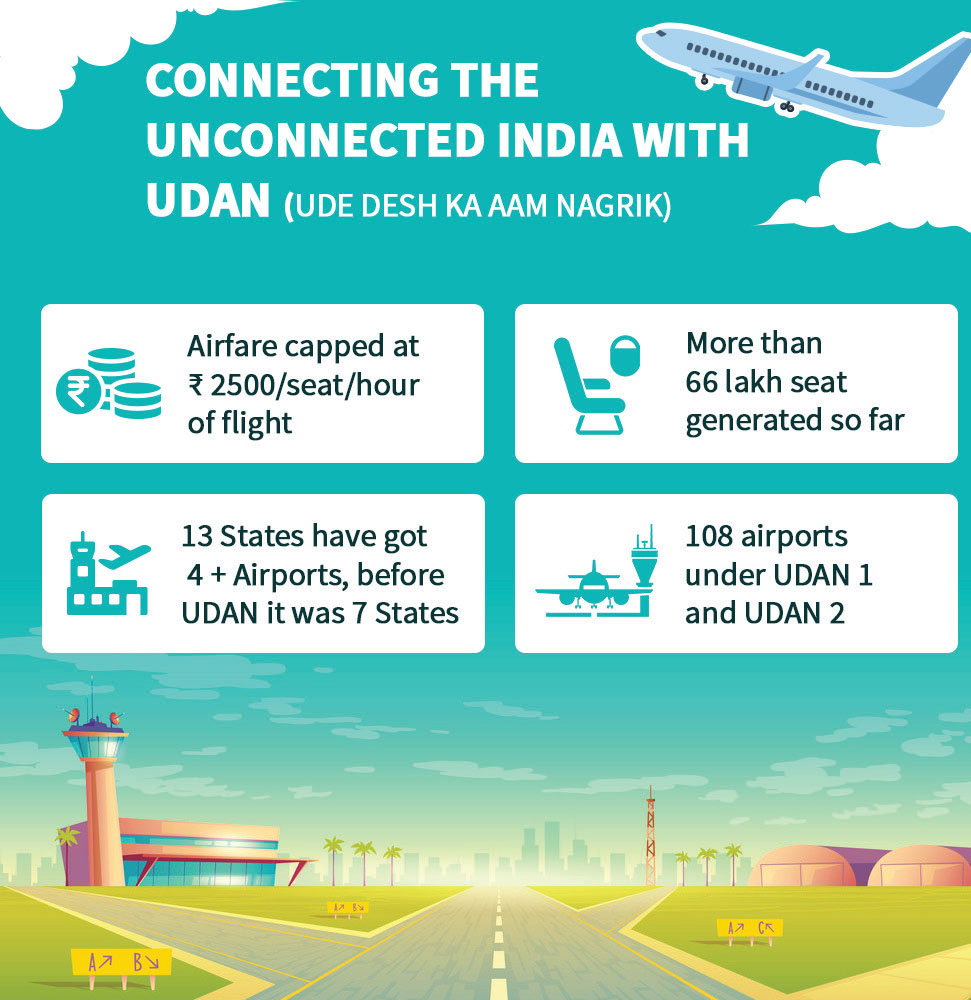

In the past decade, India has also witnessed infrastructure development on an unprecedented scale. Landmark initiatives such as PM GatiShakti, the National Logistics Policy, Bharatmala, Sagarmala and UDAN have together advanced the vision of a more connected and competitive India. As a result, over the last decade, the length of national highways has expanded by 60 per cent; 88 airports have been operationalised under UDAN; port capacity has doubled; and cargo movement through inland waterways has surged more than seven-fold. This progress has not only strengthened physical connectivity but also boosted productivity, lowered logistics costs and improved service delivery.

The services sector has remained a steady contributor to India’s growth story. It provides employment to approximately 30 per cent of the workforce. In addition, services play an increasingly vital role in the “servicification” of manufacturing, enhancing value through services used in both production and post-production stages. India’s capability in services exports is now globally recognised, especially in software and has been a major contributor to keeping the current account deficit within the sustainable level.

India has a huge comparative advantage in knowledge led activities – be it technology, services or industry 4.0. More than one- third of Indian students choose a STEM degree. In fact, India has one of the largest pools of graduates in areas of digital services, engineering, computing and data sciences in the world.

India has a huge comparative advantage in knowledge led activities – be it technology, services or industry 4.0. More than one- third of Indian students choose a STEM degree. In fact, India has one of the largest pools of graduates in areas of digital services, engineering, computing and data sciences in the world.

- Inflation Management

India formally adopted a Flexible Inflation Targeting (FIT) framework in 2016, mandating the Reserve Bank of India (RBI) to maintain inflation at 4% (+/-2%). Since then, inflation targeting has helped anchor inflation expectations, improve monetary policy credibility and enhance macroeconomic stability. In the years following the FIT adoption, headline CPI inflation largely stayed within the tolerance band, barring temporary shocks such as the food and fuel price spikes during 2019–20 and the global supply chain disruptions caused by COVID-19 and the Russia–Ukraine conflict. Importantly, inflation expectations of households and businesses have become more anchored, reducing inflation volatility and supporting long-term investment decisions. In parallel, the Government also undertook several supply side measures during this period to contain inflation. FIT, with its embedded accountability mechanism, has enabled the monetary authority to remain focused on its mandate and avoid premature policy adjustments that can be eventually counter-productive. The far-reaching impact of this reform cannot be underestimated.

- Banking Sector

The banking system is at the core of the Indian financial system, with an expanding role of non-banking financial corporations. In fact, the domestic financial system emerged stronger from the challenges posed by COVID-19 pandemic and the macro-economic volatilities caused by the war in Ukraine and the synchronised monetary policy tightening in advanced economies. Our banking sector remains strong, stable and robust, underpinned by strong balance sheets of both banks and non-banks.

Our financial markets are also rapidly maturing. Apart from the traditional sources of bank and equity financing, our entrepreneurs have a spectrum of innovative instruments like REITs/INVITs, Venture Capital and digital lending tools to meet the capital requirements for growth.

- Corporate Sector

The Indian non-financial corporate sector has also demonstrated resilience despite operating in an environment of heightened global trade policy uncertainty. According to reports, ICRA’s rating actions during the first half of the current financial year have brought out the strength of corporate balance sheets and a supportive domestic economy. The agency recorded 214 rating upgrades against only 75 downgrades during this period. Debt servicing capacity of corporates has also improved, as seen in healthy interest coverage ratios. In addition, sizeable cash buffers have strengthened corporate balance sheets. More broadly, vulnerabilities in the sector remain limited, with declining debt-to- equity ratios.

- Fiscal Sector

On the fiscal front, the Government is on a path of fiscal consolidation and debt reduction. Higher sales growth in the aftermath of the recent next-gen reforms in GST are expected to maintain and perhaps improve the revenue buoyancy of our indirect taxes.

While being on a path of fiscal consolidation, the government has placed greater thrust on capital and other developmental expenditure. For instance, three recent mega initiatives of the Government of India, namely, the Pradhan Mantri Viksit Bharat Rozgar Yojana; the Research, Development and Innovation Scheme; and the Package to Revitalize India’s Shipbuilding and Maritime Ecosystem with estimated costs of Rs.1 lakh crore, Rs.1 lakh crore and Rs.69,725 crore respectively are remarkable for their scale and expected impact.

- External Sector

India’s external sector has strengthened considerably over the last decade, owing to strong macroeconomic fundamentals, improving global competitiveness and increased openness to foreign capital. Total exports increased by 76 per cent over the last decade, led by engineering goods, electronics and pharmaceuticals. Services exports have more than doubled during this period. India’s merchandise and services exports together reached about US$825 billion during 2024-25. India’s current account deficit (CAD) has, on average, remained below 2.0 per cent of GDP over the last decade owing to robust net services exports, coupled with strong remittances counter-balancing the trade deficit.

Underpinning Structural Reforms

India’s strong performance during the last decade, as highlighted earlier and the current health of the Indian Economy are a result of various fundamental reforms carried out during this period. As I have already pointed out, Flexible Inflation Targeting Framework, 2016, has been a watershed reform which has delivered in bringing down both inflation and its volatility. Insolvency and Bankruptcy Code (IBC), 2016 has significantly strengthened the rights of creditors, improved the recovery rates, enhanced credit discipline and boosted investor confidence in India’s financial ecosystem. Real Estate (Regulation and Development) Act (RERA) – enacted in 2016 – has ushered in greater transparency, accountability and consumer protection to India’s real estate sector. Goods and Services Tax (GST), 2017 has eliminated cascading of taxes and inter-state trade barriers, streamlined the taxation process, improved the ease of doing business and encouraged formalization of the economy.

There are also a host of other structural reforms which would boost the potential of our economy. These include:

There are also a host of other structural reforms which would boost the potential of our economy. These include:

(i) High Level Committee on Non-Financial Regulatory Reforms;

(ii) Nuclear Energy Mission for Viksit Bharat targeting 100 GW nuclear power capacity by 2047;

(iii) National Critical MineralMission;

(iv) India Semiconductor Mission, and several others.

Summing up

A new sense of confidence is now palpable in the country. India’s journey towards becoming an economic powerhouse is a testament to its inherent strength and the policy initiatives of the government. A credible policy framework, with focus on multi sectoral growth, disciplined fiscal management, proactive inflation control and robust financial sector reforms, has helped the nation to build its economic strength. As India continues to pursue these reforms and adapt to the evolving global order, it is indeed well-positioned to achieve its aspiration of Viksit Bharat by 2047.

Thank You. Namaskar.

ABOUT THE AUTHOR

Shakti Kanta Das is a former IAS officer of Tamilnadu cadre; served as secretary in Ministry of Finance, served two terms as Governor of RBI; presently in the PMO as one of the two Principal Secretary to the prime minister.

Shakti Kanta Das is a former IAS officer of Tamilnadu cadre; served as secretary in Ministry of Finance, served two terms as Governor of RBI; presently in the PMO as one of the two Principal Secretary to the prime minister.