A Perspective on the Union Budget

The Union Budget 2026-2027 (Union Government’s estimated receipts and expenditure from 1.4.2026 to 31.3.2027) has been presented to the Parliament today by the Union Finance Minister, India, at 12.26 hours.

Estimated receipts of INR.36.51 trillion falls short of estimated expenditure of INR.53.47 trillion, by INR.16.96 trillion (53.47-36.51=16.96), which reflects a fiscal deficit of 4.3 percent of budgeted GDP of INR.393 trillion.

The budget estimates of fiscal deficits in the previous five years, from 2021 to 2025, were 6.5%, 6.4%, 5.9%, 4.9% and 4.4% respectively; thus, the fiscal trajectory has been on the correct path, though the pace has been rather slow ! Fiscal deficit must be curtailed to 2.5% of GDP next year. This is achievable and requires savings/generation of additional INR.7 trillion, by maintaining strict fiscal discipline.

Fiscal discipline entails overhauling the revenue collecting machinery and curtailing a bloated establishment expenditure of the Union Government (INR.8.24 trillion). This should be government’s priority number one!

Gross tax revenue is budgeted at INR.44.04 trillion; out of this, direct tax is INR.26.97 trillion and indirect tax is INR.17.07 trillion. Out of direct tax of INR.26.97 trillion, individuals contribute INR.14.66 trillion and corporates INR.12.31 trillion. Out of indirect tax INR.17.07 trillion, GST is INR.10.19 trillion, Union Excise duty is INR.3.89 trillion and Customs duty is INR.2.71 trillion, plus additional miscellaneous INR.0.28 trillion.

Gross tax revenue is budgeted at INR.44.04 trillion; out of this, direct tax is INR.26.97 trillion and indirect tax is INR.17.07 trillion. Out of direct tax of INR.26.97 trillion, individuals contribute INR.14.66 trillion and corporates INR.12.31 trillion. Out of indirect tax INR.17.07 trillion, GST is INR.10.19 trillion, Union Excise duty is INR.3.89 trillion and Customs duty is INR.2.71 trillion, plus additional miscellaneous INR.0.28 trillion.

It is noticed that income-tax to corporate-tax ratio is: 1.19: 1. This means individuals pay more direct taxes than corporates. This is inequitable; individuals must not be burdened to subsidise direct taxes to corporates!

It is commendable, however, that direct taxes (INR.26.97 trillion) are outgrowing indirect taxes (INR.17.07 trillion). Indirect taxes cause inflation. Rate of Indirect taxes may, therefore, be reduced; correspondingly, rate of corporate taxes may be increased. This exercise would be revenue neutral, while arresting inflation.

From gross tax revenue collected by Union Government, a slice is required to be distributed to the States; this is mandated by article 270 of the Constitution. The budgeted amount of INR.15.26 trillion of tax revenue to be transferred to the States is reasonable. Tax revenue distributed to States in previous 5 years from, 2021 to 2025, were INR.6.65, 8.16, 10.21, 12.47 and 14.22 trillion respectively.

These figures indicate that the Finance Commission has been discharging its Constitutional obligation reasonably well. However, cesses and surcharges must be brought into the divisible pool to boost federalism.

Non-tax revenue budgeted at INR.6.66 trillion seems optimistic. These figures in last 5 years, from 2021 to 2025, were INR.2.43, 2.69, 3.02, 5.45, and 5.83 trillion respectively. The main sources of non tax revenue are dividends and profits from Public Sector Undertakings. Focus should be directed to administer PSUs professionally with strong accountability. Rather than mopping up one time revenue from disinvestment, strengthening PSUs is a far better option. And depending on dividend from RBI to curtail revenue shortfall is retrograde.

Non-tax revenue budgeted at INR.6.66 trillion seems optimistic. These figures in last 5 years, from 2021 to 2025, were INR.2.43, 2.69, 3.02, 5.45, and 5.83 trillion respectively. The main sources of non tax revenue are dividends and profits from Public Sector Undertakings. Focus should be directed to administer PSUs professionally with strong accountability. Rather than mopping up one time revenue from disinvestment, strengthening PSUs is a far better option. And depending on dividend from RBI to curtail revenue shortfall is retrograde.

On the expenditure side, the total amount budgeted is INR.53.47 trillion. Government plans to borrow a hefty sum (32% of budgeted expenditure) to bridge revenue shortfall. Amid fiscal strain, Government’s propensity to borrow is undesirable.

Government’s burgeoning interest liability is disconcerting; the interest burden has grown from INR.8.09 trillion in 2021 to INR.14.04 trillion in 2026, reflecting an increase of 74 %. Interest burden alone wipes out corporate taxes! This is alarming!

The easy option to borrow and distribute borrowed funds must halt! Should we inundate our next generation with debt?

Impressive numbers of GDP and growth lose meaning if we are fiscally imprudent! We must recognise that a fiscally healthy India alone can become a super power! We need not wait till 2047! We have the best human resources. We only need to enforce fiscal discipline doggedly. We are failing in this area.

Fiscal Responsibility and Budget Management (FRBM) Act, 2003 was enacted by the Parliament 23 years ago; the objective was to institutionalise fiscal discipline. But what happened to this law? It has been breached systematically! And the breaches are being regularised year after year!

Charity begins at home. The Union Government must curtail its massive establishment expenditure of (INR.8.24 trillions). Establishment expenditure now exceeds India’s defence expenditure by 39%! Will it be feasible to hive off a part of the establishment and relocating it to Defence? This will trim the establishment and add heft to our defence.

Defence expenditure needs to be enhanced in view of our hostile neighbours and vitiated geo-political environment. The proposed expenditure of INR.5.94 trillion seems inadequate. This must be increased by at least INR.2 trillion.

Subsidies have been budgeted at INR.4.10 trillion; the components of subsidy are: food, fertiliser and petroleum amounting to INR.2.27 trillion, INR.1.70 trillion and INR.12,085 crores respectively. Petroleum subsidy must be enhanced considerably.

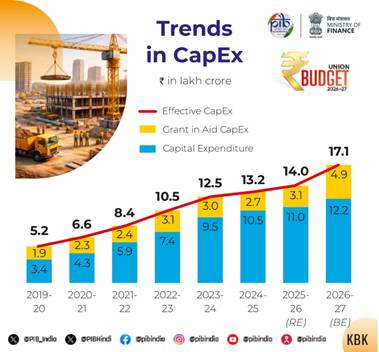

Grants in Aid for creation of Capital Assets of Union Government of INR.4.92 trillion seems adequate. Expenditure on capital account is INR.12.22 trillion is adequate. Effective capital expenditure is thus INR.17.14 trillion, which, ironically, is the approximate amount of fiscal deficit. (INR.16.96 trillion).

Pension, budgeted at INR.2.96 trillion, is a huge increase from INR.2.76 trillion last year. Pension cannot possibly be reduced, but some restraint must be exercised. This requires careful handling as the Supreme Court has ruled that pension is not a bounty but a right.

Overall, expenses for Non development expenditure are INR.37.24 trillion [14.04 (interest burden) +8.24 (establishment expenditure – 1.66 salary +2.77 pension + 4.25 other expenses), 5.94 (Defence) + 4.10 (subsidy) +4.92 (Grants in Aid of Union Government) = INR. 37.24 trillion: this leaves a residual sum of only INR.16.23 trillion. When INR.12.22 trillion of capital expenditure is deducted, we are left with only INR.4.01 trillion for development expenditure, which is inadequate for our country with a GDP of INR.393 trillion; hence the dire need to maintain strict fiscal discipline. We need to generate optimum revenue desperately.

Total debt of the union government, internal and external combined, has been budgeted at INR.215 trillion. GDP has been budgeted at INR.393 trillion. So, the Debt/GDP ratio has been budgeted at 55%. This percentage is hardly comfortable.

It is often forgotten that the backbone of the budget is tax revenue. Out of INR.53.47 trillion of total expenditure, a sum of INR.44.04 trillion is garnered from tax revenue alone! This is 82.4 % of total expenditure. All theories by economists will fail if legitimate tax revenue is denied to the government. Even today the cash economy is thriving, and, thanks to such leakage, a huge tax revenue is eluding the exchequer! India’s potential to become a superpower continues to elude her!

I remain, however, an eternal optimist, since India’s infinite spiritual power, and latent goodness hidden in each soul, is bound to manifest soon so that India’s hungry (India ranks 102 out of 123 countries in Global Hunger Index 2025) are fed adequately! This is the sacred land of Gautam Buddha and Swami Vivekananda!

ABOUT THE AUTHOR

BISHWAJIT BHATTACHARYYA is Senior Advocate, and former Additional Solicitor General of India.

BISHWAJIT BHATTACHARYYA is Senior Advocate, and former Additional Solicitor General of India.