India’s economy today is not fragile, but it is under strain in subtle ways. Growth remains intact, financial markets are upbeat, and fiscal consolidation appears to be on track. But there are emerging vulnerabilities. Oil prices, global liquidity conditions, and shifts in investor sentiment are now more significant than they were a few years ago. As William Shakespeare wrote poignantly, “The fault, dear Brutus, is not in our stars, but in ourselves, that we are underlings” (Julius Caesar, Act 1, Scene 2). The system is intact, but there are challenges on multiple fronts, necessitating a course correction.

Industrial Momentum: Encouraging, but Narrow

India’s industrial production (IIP) experienced a moderate 4.1% year-on-year growth in March 2026, marking a 5-month low, though it remains in an expansion phase. The sector showed resilience, with robust performance in manufacturing (4.3%) and capital goods (14.6%), supported by heavy infrastructure investments. The industrial sector continues to support growth, with manufacturing, infrastructure, and policy initiatives such as the Production Linked Incentive (PLI) schemes playing a central role. Core industries, viz., steel, cement, electricity, and coal, have maintained steady output. Newer segments such as electronics, pharmaceuticals, and defence manufacturing are expanding rapidly.

India’s industrial production (IIP) experienced a moderate 4.1% year-on-year growth in March 2026, marking a 5-month low, though it remains in an expansion phase. The sector showed resilience, with robust performance in manufacturing (4.3%) and capital goods (14.6%), supported by heavy infrastructure investments. The industrial sector continues to support growth, with manufacturing, infrastructure, and policy initiatives such as the Production Linked Incentive (PLI) schemes playing a central role. Core industries, viz., steel, cement, electricity, and coal, have maintained steady output. Newer segments such as electronics, pharmaceuticals, and defence manufacturing are expanding rapidly.

But the pattern of growth raises questions. Most expansion is concentrated in capital-intensive areas, viz., electronics assembly, renewable equipment, and advanced manufacturing, rather than sectors that create large-scale employment. Output is rising, but job creation is lagging. April 18, 2026, issue of the EPW demonstrates a dualism in “India’s manufacturing sector with a large number of unorganised enterprises but accounting for a substantial proportion of value added”.

India’s approach also differs from the export-led industrialisation seen in East Asia. Growth remains largely domestic and policy-supported. Private investment has improved, but it is not yet broad-based. High borrowing costs, input price pressures, and uncertain global demand continue to weigh on smaller firms.

India’s approach also differs from the export-led industrialisation seen in East Asia. Growth remains largely domestic and policy-supported. Private investment has improved, but it is not yet broad-based. High borrowing costs, input price pressures, and uncertain global demand continue to weigh on smaller firms.

Capacity utilisation is rising, though unevenly across sectors. Technology-driven industries are pulling ahead, while traditional manufacturing is slower to recover. For now, industrial growth appears cyclical rather than transformational.

Fiscal Consolidation: Progress with Caveats

The government’s discernible progress is reflected in projected decline to 4.3% of GDP by FY 2026-27, supported by strong tax collections and controlled spending growth. Public capital expenditure, now over ₹12 lakh crore, remains a key pillar of policy.

The durability of this consolidation, however, depends on several assumptions. Continued growth, stable oil prices, and steady revenue performance are all built into the outlook. Meanwhile, structural expenditures on food security, rural employment, and fertilisers limit flexibility. These are not easily reduced.

External factors exacerbate the uncertainty. Higher oil prices can quickly raise subsidy costs and widen fiscal pressures. Fertiliser subsidies tend to rise sharply in such periods.

While a small deviation may not be problematic, repeated slippages could gradually weaken fiscal credibility. State finances add another layer of complexity, especially given off-budget liabilities in sectors like power and infrastructure, necessitating a credible fiscal framework.

External Balance: Cause for Concern, not Alarm

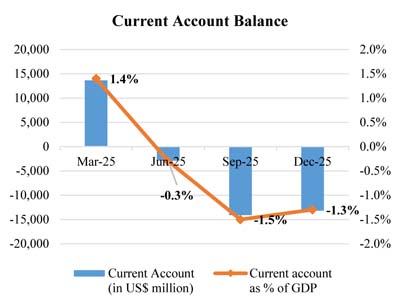

India’s external position remains manageable. The current account deficit (CAD) is likely to stay below 1% of GDP in FY 2025-26, supported by strong services exports and remittances. However, this stability depends heavily on oil prices. The trade deficit continues to be driven by energy imports and electronics. A sustained rise in crude prices would quickly change the picture. Historically, large increases in oil prices have made the CAD disconcerting.

Foreign exchange reserves provide a cushion, and capital inflows have remained supportive. But both are sensitive to global financial conditions, particularly interest rates and risk appetite. Thus, the external sector is stable but susceptible to global headwinds.

Equity Markets: Strong, yet Partially Stretched Valuations

Equity markets reflect optimism about India’s growth prospects. Corporate earnings have been robust, and domestic investors have played an increasingly important stabilising role, though valuations in some sectors are stretched. Market gains are concentrated in a relatively small group of large companies, while mid- and small-cap stocks have shown bouts of volatility, suggesting some imbalance. Markets are pricing in long-term potential, but may be underestimating near-term risks, especially those linked to global conditions and input costs.

Equity markets reflect optimism about India’s growth prospects. Corporate earnings have been robust, and domestic investors have played an increasingly important stabilising role, though valuations in some sectors are stretched. Market gains are concentrated in a relatively small group of large companies, while mid- and small-cap stocks have shown bouts of volatility, suggesting some imbalance. Markets are pricing in long-term potential, but may be underestimating near-term risks, especially those linked to global conditions and input costs.

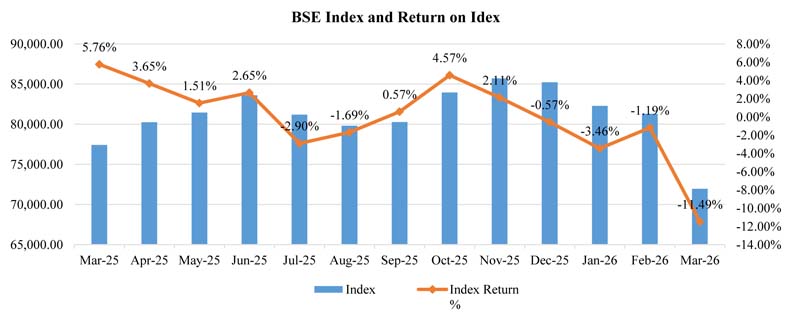

The escalation of the West Asia crisis triggered a sharp global equity sell-off, with Indian markets also witnessing significant declines amid rising crude prices and record FPI outflows. The Nifty 50 fell to a 13-month low, declining 11.3% in March, while the Sensex dropped 11.5% to a more-than-two-year low. The correction was broad-based, with midcap and smallcap indices falling over 10% and major sectors such as banking, auto, and realty witnessing steep losses. Banking stocks were further hit by governance concerns, amplifying market weakness. Despite the sharp correction, valuations turned attractive, with benchmark indices trading at multi-year lows in P/E terms.

The Rupee: Gradual Adjustment

The Rupee: Gradual Adjustment

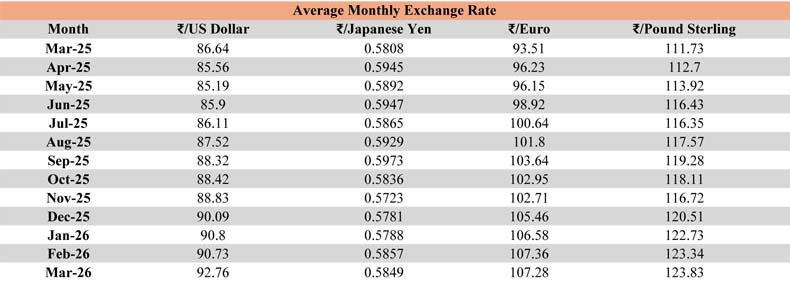

The Indian Rupee has weakened in a relatively orderly manner into the mid-90s against the US dollar, reflecting higher import costs, tighter global liquidity, and sustained capital outflows, further exacerbated by the West Asia crisis and rising crude prices. It depreciated by 2.2% in March to an average of ₹92.76/US$, the sharpest monthly fall in over three years, and touched a low of ₹94.65/US$ by month-end. While a weaker currency offers some export support, it raises import costs and inflationary pressures, with RBI interventions to stabilise the currency leading to a US$ 40 billion drawdown in forex reserves to US$ 688 billion.

Oil and Precious Metals: Key Indicators

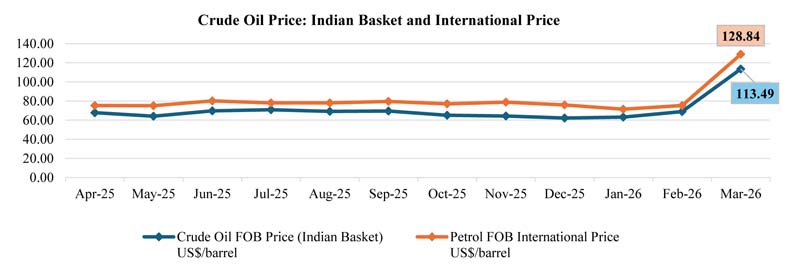

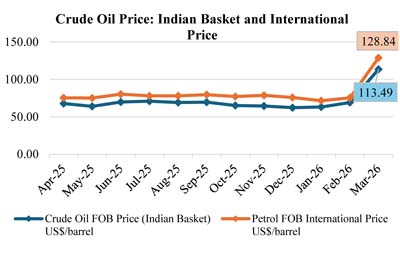

Oil continues to be the most important external variable for India. Higher prices have an economy-wide impact on inflation and fiscal balances on household consumption. Crude oil (Indian basket) and petrol FOB prices remained broadly stable through April 2025-February 2026, with crude largely in the range of $62-71/bbl and petrol around $71-80/bbl. A sharp spike is observed in March 2026, with crude rising to $113.5/bbl and petrol to $128.8/bbl, indicating a significant global price shock. The widening price levels suggest strong pass-through from crude to refined product prices, reflecting heightened volatility in energy markets.

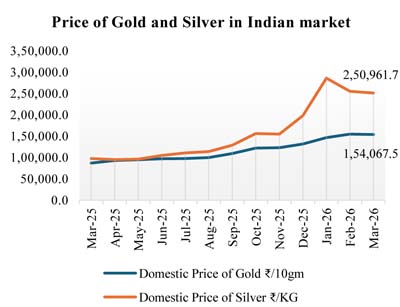

Gold and silver prices also offer signals about global uncertainty. When these rise, it often reflects concerns about inflation or geopolitical risk. For India, higher gold imports can widen the trade deficit and shift savings away from financial assets. These factors tend to reinforce each other, amplifying external pressures.

Overall Assessment: Strengths and Fault-Lines

India’s economic position is resilient, but all is not well on the external front. Industrial growth is strong, fiscal consolidation is on track, CAD is modest by historical standards, equity markets are buoyant, and the rupee’s depreciation remains controlled rather than disorderly. Then, India is not facing a crisis; it is not “a riddle wrapped in a mystery inside an enigma…” (Winston Churchill, October 1939 radio speech).

It is, however, entering a phase where external conditions matter more, and policy choices carry greater weight since the overall landscape is hugely dependent on high oil prices not rising further, on continued services-export strength, and on political discipline to sustain fiscal consolidation in a challenging global environment.

Sustaining growth requires broader and more employment-intensive industrial growth and higher productivity, improved external resilience through sustained reserve accumulation, diversification of export markets, and a continued push for renewables to reduce oil intensity, and credible and adaptable fiscal and monetary policies that anchor inflation expectations even as the state continues to support infrastructure and social spending.

The challenge calls for resilience reminiscent of Lord Alfred Tennyson’s immortal lines in Ulysses: “To strive, to seek, to find, and not to yield.” The verse encapsulates a philosophy of perseverance, a refusal to be constrained by circumstances or momentary setbacks.

In sum, India’s macro story remains comparatively attractive among large emerging markets. But the triple whammy of expensive oil, a weakening rupee, and elevated gold and silver prices reveals burgeoning external and inflation risks. India’s current economic position manifests a dynamic interplay of growth, stability, external balance, market sentiment, and commodity dependence, a system striving to balance expansion with caution.

An incisive examination of the State of the Economy published in Reserve Bank of India Bulletin – April 2026, justifiably held, “The strong macroeconomic fundamentals should support the Indian economy to maintain its resilience to withstand such shocks”. I have repeatedly substantiated this thesis in my writings, speeches, and interviews.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.