“It is not the strongest of the species that survives, nor the most intelligent, but the one most adaptable to change”. Charles Darwin

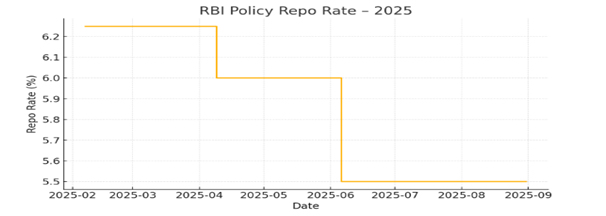

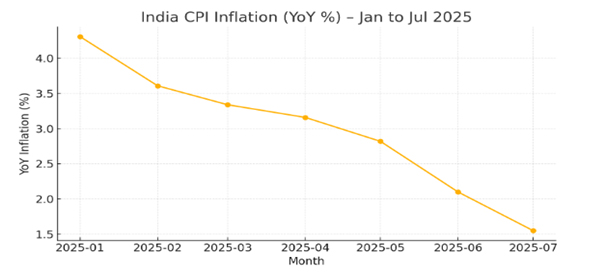

The Monetary Policy Committee (MPC) unanimously voted to maintain the repo rate at 5.50% and to continue a neutral stance at its 56th meeting (August 4–6, 2025). This policy was formulated against the backdrop of Trump’s tariff tirade, global financial market volatility, stable 6.5 % macroeconomic growth in FY 26, and inflation slackening to a 77-month low of 2.1 % in June, and a benign inflation outlook.

Case for the RBI’s Pause

Given such global cues and the domestic economic setting, the RBI appropriately held the policy repo rate steady at 5.50%. Key elements in the MPC’s rationale included a benign inflation trajectory, though upside risks (oil price movements, exchange rate swings, supply constraints) were also flagged; growth-inflation balance; liquidity and transmission progress; and heightened external uncertainties and geopolitical risk. The decision not to surprise markets or implement a surprise move after three consecutive rate cuts totalling 100 basis points since February, and maintaining the policy stance as “neutral”- as in June- after briefly turning “accommodative” in April, is a positive step.

The MPC’s measured pause — rather than immediate further easing — occurred against the backdrop of subdued headline inflation (well below the RBI’s medium- term target midpoint, though disinflation was mainly driven by transient food price movements, and food price volatility could reverse), relatively resilient GDP growth forecasts, and external uncertainty from tariffs and exchange rates. There was also a need to incorporate the earlier easing and the forthcoming CRR easing into the system and to monitor the external shock before initiating further rate action.

Some naysayers emphasized the low inflation prints to maintain that the RBI had room to cut further to support growth proactively. If low inflation proves durable, delay risks missing an opportunity to shore up demand — especially for investment — in a year when external demand may slacken. The immediate hit to GDP from tariffs was uncertain but material; letting the monetary transmission play out and CRR injections operate, avoiding oversteering and preserving policy ammunition if inflation reverses. The RBI must also consider financial stability implications and the uneven transmission of cuts to borrowers. Overall, given the twin facts of low retail inflation and a sudden external shock (tariffs) that primarily affects demand and foreign exchange, a cautious pause that leaves room for both further easing (if data permit) and intervention (if foreign exchange pressures intensify) was prudent.

The MPC emphasised data dependence and flagged that future action would hinge on evolving inflation dynamics, growth momentum, and external conditions. The RBI also signalled readiness to deploy forex reserves and liquidity tools if required.

Global Setting: Geopolitics, Commodities, and External Financial Conditions

The global growth, which remains uneven, is marked by trade shocks, geopolitics, and monetary divergence. Advanced-economy central banks have continued to normalise policy in recent years, and although headline disinflation in many advanced economies has provided scope for easing expectations, growth risks remain from policy uncertainty and uneven demand. Commodity price volatility (especially oil) tied to geopolitics and demand shifts clouds the inflation outlook.

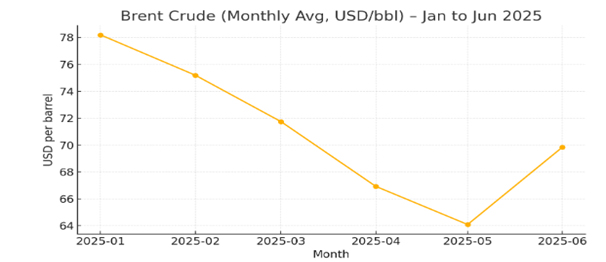

Geopolitics, particularly U.S. trade actions, suddenly acquired centre stage in early August 2025. The U.S. administration announced substantial tariffs targeted at India tied to India’s handling of Russian energy purchases. This sharply elevated bilateral tensions and created an immediate downside risk to Indian exports, manufacturing confidence, and capital flows. This development highlighted the risk of export displacement, supply-chain adjustments, and lost incomes for export-intensive sectors. The markets reacted unevenly: commodity markets (notably crude oil) were initially apprehensive but then largely looked through the immediate policy shock, while risk premia around trade-sensitive sectors rose.

The tariff announcement was not a standard macroeconomic shock; it was geopolitical, politically timed, and could evolve rapidly, thereby complicating medium-term external risk assessments. For emerging markets like India, such geopolitical trade shocks matter via several channels: direct trade disruptions, commodity price transmission (imported inflation risk), portfolio flows, and risk sentiment. If tariff measures persist or escalate, they could dampen export-oriented sectors and heighten uncertainty for investment and external receipts. Simultaneously, the immediate market reaction to oil prices was muted, reflecting market expectations that such measures might be temporary or politically reversible. Nonetheless, the risk that tariff-driven trade tensions could raise certain commodity prices and disrupt supply chains disconcerted monetary policymakers.

The tariff shock for Indian is asymmetric: it primarily threatens specific export lines (textiles, light manufactures, and some processed goods) and hurts foreign earnings and investor sentiment in the near term. This external shift affects traded price inflation, exchange rates, and capital flows. There were some indications that the RBI was active in forex markets in early August to steady the rupee.

India’s Domestic Landscape- Growth, Inflation, Fiscal and External Balances

In this uncertain global environment, India has outperformed with a steady, high-growth trajectory. The World Bank estimates that the Indian economy grew by 7.1% in 2024-25, maintaining its position as the fastest-growing major economy for the fourth year in a row. This performance was driven by strong domestic demand, continued government-led capital investments, and resilient services exports. Fiscal-year GDP growth for FY 25 and quarterly indicators suggest that domestic demand had retained momentum: private consumption and investment continued to be the growth engines, and services and construction activity remained robust, thereby supporting continued employment generation and revenue buoyancy. The RBI retained its FY26 real GDP growth forecast at 6.5% reflecting resilient domestic demand, continued progress in services and consumption, and underlying investment activity in select sectors despite external headwinds. The forecast implies confidence that domestic demand will cushion the effects of the trade shock at the aggregate level, but sectoral dislocations are likely.

The Flexible Inflation Targeting Framework (FITF) was introduced in India post the amendment of the RBI Act in 2016. Per the RBI Act, the Government of India sets the inflation target every five years with the RBI’s consultation. The inflation target has been mandated by the RBI Act, amended through the Finance Act, 2016, to be 4 % (+/-2 %).

A striking feature of India’s macro backdrop in mid-2025 has been the persistent and faster-than-expected decline in headline inflation. CPI inflation fell into single digits, well below the RBI’s medium-term tolerance band, with month-on-month and year-on-year prints declining for several months. India’s headline CPI inflation has been plummeting, with CPI inflation decelerating to a 77-month low of 2.1% in June 2025, driven largely by favourable base effects and supply improvements (monsoon, reservoir levels, buffer stocks). Accordingly, the RBI pared its FY26 CPI projection to around 3.1% (with quarterly skews showing a likely rise later in the fiscal year). While low inflation makes for easier policy, the RBI explicitly noted that volatile food prices and potential imported inflation (from oil or through exchange rate pass-through) remain risks.

India’s fiscal position in FY 25 showed continued consolidation efforts alongside elevated capital expenditure pushes. The combination of buoyant nominal GDP growth and revenue collection helped fiscal arithmetic, but aggressive monetary easing in the face of loose fiscal policy can stoke second-round inflationary effects. The trade and current account balances remained manageable, though susceptible to oil price movements and exports. The sudden U.S. tariff move added a downside risk to the export outlook and introduced uncertainty into the external receipts’ trajectory.

The 2025–26 fiscal stance at the central and state levels remains mildly expansionary relative to the post-pandemic glide path — infrastructure and capex commitments continue, which supports demand. The RBI’s policy thus faces a classical trade-off: accommodative settings help growth but reduce the policy headroom to fight any future surge in inflation. The immediate tariff episode raised concerns about export receipts and capital flows. The pressure on the rupee suggested RBI intervention in forex markets to provide stability. The RBI’s exchange reserve position and interventions, along with market expectations, became central to the near-term outlook.

Banking System Liquidity and Transmission

By August 2025, the Indian banking system was operating with ample surplus liquidity. The RBI’s operations and the evolving domestic fiscal calendar caused a pronounced surplus under the Liquidity Adjustment Facility (LAF), with average daily surpluses ranging between roughly ₹3.0 lakh crore and close to ₹4.0 lakh crore, depending on the window used. The RBI had also used market operations, including open market purchases, repos, and forex operations, to manage intra-day and structural liquidity. The maturity and potential non-renewal of certain swap operations were expected to drain some liquidity in the near term, but systemic surplus persisted. A surplus environment tends to compress short-term money market rates and facilitate the pass-through of policy easing to market rates. In 2025, the RBI had front-loaded the easing, with cumulative repo reductions (including a 50 bps cut in June) and 100 bps phased Cash Reserve Ratio (CRR) cut (from 4% to 3% in four tranches) to release ≈ ₹2.5 lakh crore of primary liquidity (phased through Sep–Nov 2025) were announced to inject durable liquidity into the banking system, ease funding conditions, and support credit flow. Transmission was reflected in declining fresh loan rates, and reducing deposit rates, albeit with the usual lags and heterogeneity across bank balance sheets. The fall in lending rates on new loans and the decline in deposit rates since the prior policy turn indicate that earlier easing was filtering into borrowing.

Transmission, however, remained incomplete and uneven; smaller banks and certain segments of the market continued to price in higher spreads, reflecting liquidity management preferences, funding mix, and competitive dynamics. The lagged effect reflects balance-sheet frictions, non-bank financing variability, and banks’ risk appetites. The RBI’s August pause, therefore, signalled that it wanted to allow the full effect of earlier cuts and the CRR glide-path to percolate through before committing to further rate moves.

The pause had immediate effects on bond yields and money market rates: markets interpreted the hold as signalling the end (or at least a pause) to the active easing cycle until the RBI sees clearer evidence on inflation and external stability. Yields were somewhat volatile, influenced also by global sentiment tied to the tariff shock.

The credit-deposit ratio for the banking system at end-June 2025 was 78. 9%. Bank credit grew at 12. 1% during FY 25, slower than the 16. 3% growth in FY 24. The flow of non-food bank credit during FY 2024-25 decreased by about ₹ 3. 3.4 lakh crore from ₹ 21. 4 lakh crore to nearly ₹18 lakh crore. Overall financial resource flow to the commercial sector increased from ₹ 33. 9 lakh crore in 2023-24 to ₹ 34. 8 lakh crore in 2024-25. With persistent surplus liquidity of approximately ₹ 2. 8 lakh crore, the RBI is considering reforms to the liquidity framework, such as a new 7-day VRR (Variable Rate Repo), a review of the fixed-rate repo window, and the introduction of SORR (Secured Overnight Reference Rate).

Risks, channels, and sectoral implications

Trump’s tariff tirade will hit hard the exports of textiles, some engineering goods, processed foods, etc. Even if the aggregate GDP impact is moderated by domestic demand, concentrated job and investment risk exist in export-oriented clusters. The US’s tariff action could reduce GDP growth by 30 bps and export growth by 80 bps. Inflation risk emerges via the exchange rate and oil. Rupee depreciation would raise imported inflation, especially if oil or commodity prices tick up. This channel could offset the current food-led disinflation and make future cuts less likely.

There are also implications for financial stability and credit. A weakening growth outlook combined with sectoral stress could erode asset quality in banks’ portfolios in vulnerable sectors. The RBI will therefore balance the desire to support growth with the need to preserve financial stability. Liquidity measures (CRR cuts) are designed to ease funding for creditworthy demand while giving the RBI the ability to tighten if needed.

Future Monetary Action

Moving forward, the RBI, with its data-driven and evidence-based policy approach in respect of (i) CPI prints (especially food and core), (ii) transmission of earlier cuts into MCLR and corporate borrowing rates, (iii) credit growth and bank deposit trends, (iv) forex reserves and rupee behaviour, and (v) the trajectory of export orders and manufacturing PMI, may cut the rate in October 2025, provided soft inflation persists and external shocks diminish.

Headline CPI is low, but with risks from food volatility and imported inflation, a further immediate cut in the repo rate is not ruled out. The RBI will factor in inflation prints, the transmission of previous easing to bank lending rates, and forex/export developments in its decision-making matrix. If tariffs disrupt crude flows and force up global oil prices, inflation could re-accelerate and necessitate a quicker withdrawal of accommodation.

Developmental and Regulatory Policies

The three key consumer-centric announcements- focusing on micro insurance and pension schemes for financial inclusion and customer grievance redress; standard procedures for settling death claims and articles in bank lockers; and retail participation in treasury bills through systematic investment plans (SIPs)- are well-conceived.

Concluding Observations

The RBI’s August 2025 decision to stay the course underscores the RBI’s insistence on monitoring the evolution of disinflation and the potential impact of a large external shock. Markets should expect conditional policy moves, not a mechanical timeline, because of inflation prints, oil and commodity prices, liquidity dynamics, and the ramifications of disruptive tariff moves. The CRR glide-path and liquidity operations show that the RBI continues to use balance-sheet tools alongside interest-rate policy to support credit and manage liquidity. This Policy toolkit transcends rates and provides flexibility.

External shocks can overwhelm domestic narratives. Even when domestic inflation is benign, geopolitics (tariffs, sanctions, oil politics) can force central banks to be cautious. For India, the new tariff episode heightens the need for agile macro management and a coordinated fiscal-monetary approach to support affected sectors while maintaining price stability.

Given the evolving growth-inflation dynamics, the RBI made the right decision. Ultimately, the effectiveness of the RBI’s multi-instrument approach will be judged by whether monetary easing and CRR move translate into credit availability and improved real economic outcomes without inflationary flare-ups.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.