The heightening United States–Israel–Iran conflict of 2026 marks a decisive escalation in West Asian geopolitics, transforming what initially appeared as a limited military engagement into a full-scale regional confrontation with global ramifications. The conflict formally began on 28 February 2026 with coordinated strikes by the United States and Israel targeting Iranian military installations, nuclear facilities, and senior leadership nodes across Iran. Since then, it has evolved into a complex, multi-domain theatre involving air, sea, cyber, and proxy theatres, signalling a dangerous expansion beyond bilateral hostilities.

This cycle of destruction reflects a rapid escalation into a wider regional war. Thousands of aerial and missile strikes have been carried out on Iranian territory, with Iran retaliating through sustained missile and drone attacks on Israeli cities and American military bases across the region. Maritime tensions have intensified in the strategically crucial Strait of Hormuz, through which nearly one-fifth of global oil supplies pass, leading to disruptions in energy flows and heightened insecurity in international shipping lanes. The targeting of energy infrastructure has further deepened the crisis, with Israeli strikes on the South Pars gas field provoking Iranian retaliation against Gulf-based oil and gas facilities. Simultaneously, the conflict has spilt over into neighbouring theatres, with Hezbollah and Iran-backed militias engaging Israeli and U.S. interests across Lebanon, Iraq, and the Gulf region.

With oil prices surging past $119 per barrel and military operations intensifying, the conflict has unmistakably moved beyond the confines of a limited war into the dangerous terrain of a regional conflagration. What is prognostically alarming is the ominous prospect that further escalation could spiral into a full-scale global war, with devastating repercussions for the global economy at large and the Middle East in particular. Such short-sighted and myopic policies undermine the very foundations of a rules-based international order.

The strategic positions of the principal actors reveal clarity of intent and inherent contradictions in the escalation of violence igniting into a wider conflagration. The United States seeks to degrade Iran’s military capabilities, particularly its missile, drone, and naval disruption capacities, while simultaneously ensuring the security of global energy routes and avoiding a prolonged ground war. This reflects a calibrated “limited war” doctrine, wherein aerial and naval superiority is leveraged without committing to occupation. However, the U.S. approach is marked by internal tensions, as it supports Israeli offensives while remaining cautious about attacks on critical energy infrastructure due to the risk of triggering a global economic crisis.

Israel has, however, adopted a far more expansive and aggressive posture. Its strategy is centred on the pre-emptive neutralisation of Iran’s nuclear and missile capabilities, combined with targeted strikes on economic assets such as the South Pars gas field. Although officially denying intentions of regime change, Israeli rhetoric and operational depth suggest a broader objective of permanently weakening Iran as a regional adversary. Claims of having destroyed a substantial portion of Iran’s missile launch infrastructure underscore Israel’s pursuit of decisive and transformative military outcomes.

In contrast, Iran’s strategy is rooted in asymmetry and endurance. Despite suffering significant losses, it has responded through sustained missile and drone warfare, cyber operations, and the activation of its extensive network of regional proxies. Organisations like the Islamic Revolutionary Guard Corps have consolidated domestic power, ensuring regime stability even under intense external pressure. Iran’s targeting of energy infrastructure in the Gulf reflects a deliberate attempt to raise the global economic costs of the conflict, thereby exerting indirect pressure on its adversaries. Rather than seeking outright victory, Iran appears focused on regime survival, deterrence, and forcing negotiations on favourable terms, effectively waging a protracted war of attrition.

In terms of duration, while initial Israeli assessments suggested a short conflict lasting three to six weeks, structural realities point towards a much longer trajectory. Iran’s capacity for asymmetric warfare, its reliance on proxy networks, the absence of any immediate prospects of regime collapse, and the high strategic stakes surrounding its nuclear programme all indicate that the conflict is unlikely to end swiftly. At the same time, certain constraints, such as, mounting global pressure due to rising energy prices, the United States’ reluctance to engage in a ground invasion, and the economic strain on all parties, may prevent a full-scale, prolonged war. Consequently, the most plausible scenario is a protracted, low-intensity conflict extending over months or even years, punctuated by intermittent phases of high-intensity escalation, a pattern characteristic of earlier conflicts in West Asia. For, as Carl von Clausewitz said, “War is a continuation of politics by other means”.

Global Ramifications- Wide and Profound Consequences

Grim portents abound. The significant scaling back of American policy architecture and operational framework marks a watershed moment in global history reminiscent of William Shakespeare’s powerful observation in his classic play, Hamlet, “Though this be madness, yet there is method”. In case of such sweeping onslaughts, the jury is still out on whether there is a method in the madness, and there is widespread concern and consternation about the implications of such measures.

The global implications of this war are profound and multidimensional. Politically, the conflict signals a weakening of the rules-based international order, as pre-emptive strikes and violations of sovereignty become increasingly normalised. The emergence of bloc politics, with the United States and Israel on one side and Iran potentially drawing tacit support from powers like Russia and China, points towards a more polarised and conflict-prone international system. Additionally, the prominence of non-state actors such as Hezbollah underscores the growing importance of hybrid warfare and the erosion of state-centric security frameworks.

Economically, the war’s impact is immediate and severe. The disruption of oil and gas supplies, coupled with instability in the Strait of Hormuz, has triggered sharp increases in energy prices, with the possibility of reaching $150 per barrel if hostilities persist. This has cascading effects on global supply chains, inflation rates, and economic growth. Energy infrastructure attacks reveal the vulnerability of global energy systems, while stock market volatility reflects heightened uncertainty. For energy-importing countries like India, the consequences are particularly acute, manifesting in rising import bills, pressure on fiscal balances, and widening current account deficits.

Diplomatically, the conflict has dealt a severe blow to multilateralism. Negotiations surrounding Iran’s nuclear programme have effectively collapsed, and institutions such as the United Nations appear increasingly marginalised in crisis resolution. In their place, new mediating actors such as Qatar and Turkey are attempting to facilitate dialogue, while China’s diplomatic engagement reflects its growing global ambitions. Meanwhile, Gulf states face complex strategic dilemmas, balancing their security partnerships with the United States against the imperative of regional stability, and Europe’s concerns over energy security are intensifying.

From a security perspective, the war is normalising the use of energy infrastructure as a tool of warfare, marking a dangerous shift in strategic practice. The increasing role of cyber operations and hybrid conflict further complicates traditional notions of warfare, while the spectre of nuclear escalation, though still a low-probability scenario, cannot be entirely dismissed given the stakes involved.

A critical evaluation of the conflict reveals inherent contradictions and deep fissures. Tactical military successes, particularly by the United States and Israel, have not translated into clear strategic outcomes, as the Iranian regime remains intact and resilient. Short-term gains risk producing long-term instability by entrenching hardline elements within Iran and expanding the geographical scope of the conflict. At the same time, Iran’s strategy of resistance, while effective in sustaining the conflict, carries the risk of severe economic deterioration and further international isolation. The weaponisation of energy resources also undermines the foundations of globalisation, exposing structural vulnerabilities in the interconnected global economy.

In sum, the 2026 United States–Israel–Iran war represents a watershed moment in contemporary geopolitics. Far from being a confined regional conflict, it constitutes a systemic shock with far-reaching implications for global political alignments, economic stability, and diplomatic norms. The absence of a clear path to decisive victory suggests that the conflict will persist in various forms, reshaping the international order towards greater fragmentation, volatility, and strategic competition, with consequences that extend well beyond West Asia. As the problems get worse, the stakes rise higher, necessitating an end to this war, which is fraught with devastating consequences not just for the Middle East but also for the world at large.

Debilitating Macroeconomic Impact- No Country Is an “Island in the Stream” (Ernest Hemingway)

India’s precarious position in a fractured energy world presents a multidimensional challenge—threatening energy security, remittance stability, trade and capital flows, investor confidence and macroeconomic momentum—just as the economy appeared to have entered a “Goldilocks Zone” of low inflation, narrowed current account deficit (CAD), and strengthened GDP growth. This assumes greater significance in the case of industries, such as energy, infrastructure, and manufacturing, which are sensitive to international trade dynamics and supply chain disruptions.

Few major economies are as structurally exposed to external energy shocks as India. The country imports nearly 88% of its crude oil, about 50% of its natural gas, and close to 60% of its LPG requirements. This heavy import dependence, combined with geographic concentration of supply, renders India uniquely vulnerable to disruptions in the Persian Gulf. Nearly half of India’s LNG imports originate from a single supplier, Qatar, further amplifying this concentration risk.

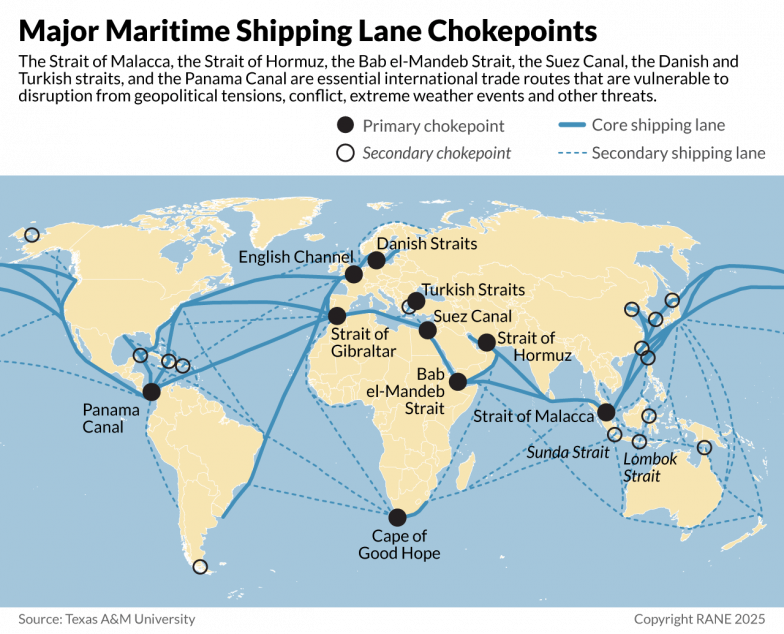

Crisis in the Strait of Hormuz: Small Passages, Big Stakes

In my writings and speeches over the years, I have repeatedly demonstrated that the proximity of the Strait of Hormuz to the UAE, Dubai, Saudi Arabia, and Qatar, along with the potential for conflict escalation to Yemen and the Strait of Bab El-Mandeb, creates a geoeconomic dependency asymmetry, particularly for Asian growth markets in general and India in particular. The ongoing conflict involving Iran has transformed the Strait of Hormuz from a strategic chokepoint into a contested war zone. What began with ambiguous geopolitical objectives has now crystallised into a singular global priority: reopening this vital maritime artery. Yet, despite calls for collective intervention, major powers remain hesitant, leaving global shipping in a state of uncertainty often described as a “wild west.”

For India, the consequences are immediate and tangible. Over twenty Indian-flagged vessels carrying crude oil, LNG, and LPG remain stranded, unable to transit the strait. These ships collectively hold millions of tonnes of energy supplies critical for domestic consumption. While diplomatic and logistical efforts are ongoing, the unpredictability of the situation underscores the fragility of India’s energy lifelines.

Energy Security Under Stress

India initially managed to cushion crude supply disruptions by diversifying imports toward Russia, West Africa, the United States, and Latin America. However, this strategy has clear limits. Unlike crude oil, natural gas and LPG are far less fungible, with infrastructure constraints making rapid substitution difficult. Consequently, industrial and commercial gas supplies have already been curtailed, raising concerns about production slowdowns and cost pressures. The deeper structural issue is stark: before the conflict, more than half of India’s crude imports—and up to 95% of its LPG—depended on routes passing through the Strait of Hormuz. The current disruption, therefore, strikes at the core of India’s energy security architecture.

Energy as a Weapon

The conflict has entered a more dangerous phase, where energy infrastructure itself has become a direct target. Attacks on gas fields, refineries, and export terminals have transformed oil and gas from commodities into instruments of geopolitical warfare. With oil prices surging sharply, gas prices, especially in Europe, spiking, and supply chains across continents facing disruption, global repercussions are starkly visible. This marks a fundamental shift—from concerns about transit security to systemic risks to energy production itself.

Macroeconomic Shock Transmission -What, How and Why

For India, this crisis represents a classic external shock transmitted through multiple channels:

1. Commodity Price Vulnerability

Energy prices remain the single largest swing factor for India’s macroeconomic stability. Rising crude prices widen trade deficit, current account deficit, and fiscal deficit.

2. Global Demand Uncertainty

A slowdown in major economies (U.S., Europe, China) could dampen demand for Indian exports, particularly, discretionary goods, and intermediate manufacturing inputs.

3. Exchange Rate Pressures

A weaker rupee increases the cost of imports, especially oil and gold, fueling inflationary pressures.

4. Logistics and Trade Disruptions

Shipping delays and rerouting increase costs, disrupt supply chains, and strain working capital cycles.

Foreign Trade Exposure

The Gulf–Levant region accounts for ~15% of exports and ~21% of imports. This trade is concentrated in high-value sectors, such as energy, precious metals, and electronics. Export risks are unevenly distributed across regions gems and jewellery (Surat, Jaipur, Mumbai), apparel (Tiruppur), automobiles (Ahmedabad), and electronics (Kanchipuram, Kolar). Perishable exports, such as grapes, bananas, and meat, face acute risks from delays. With thousands of exporters and importers dependent on Hormuz-linked routes, the disruption threatens payment cycles, production continuity, and business viability.

Currency Volatility: A Structural Story

The rupee’s fall past ₹93 per dollar on March 20, 2026, on heightened worries over the hit from the Iran war-led disruption of global energy supplies has triggered concern. But a longer-term perspective reveals continuity rather than crisis. Historically, the rupee has depreciated at an average rate of 3.5–4% annually, reflecting structural economic dynamics. The recent decline, however, has been accelerated by rising oil import bills, weak capital inflows, global risk aversion, and higher U.S. interest rates.

An important nuance lies in the Real Effective Exchange Rate (REER). While the rupee may weaken against the dollar, its competitiveness depends on movements against a basket of currencies adjusted for inflation. Thus, nominal depreciation does not automatically imply a loss of trade competitiveness.

Markets in Turmoil

Financial markets reacted sharply to the crisis. This was clearly manifested in equity indices falling over 3% in a single session, oil prices surging past $110 per barrel, and the rupee hitting record lows. War doesn’t just affect borders; it affects oil, currencies, and liquidity. And ultimately, it affects earnings, multiples, and market direction. The sell-off reflects a “perfect storm” of geopolitical escalation, rising energy prices, and tight global financial conditions. Foreign investors, drawn by higher U.S. yields, have begun reallocating capital away from emerging markets like India.

Inflationary Pressures

Oil remains the primary transmission channel for inflation. Every $10 increase in crude adds ~0.2–0.4 percentage points to inflation. Higher fuel costs cascade into transport and production costs. The central bank may be forced to delay rate cuts and maintain a tighter monetary stance.

Fuel Shortages and Structural Gaps

The LPG shortage highlights a critical structural weakness. Unlike crude oil, where India maintains strategic reserves, LPG systems are designed for continuous flow rather than storage. With over 85% of LPG imports passing through Hormuz and limited backup storage, supply disruptions quickly translate into shortages and household consumption is directly affected. This exposes a key policy gap of the absence of long-term LPG storage infrastructure.

A Question of Perspective

Despite these challenges, it is important to retain a sense of proportion. In comparison to several countries in the region grappling with active military conflict, widespread infrastructure destruction, and deep systemic instability, India’s situation, though serious, remains within the bounds of manageability.

A useful analogy may help clarify this distinction: while some nations are in intensive care, fighting for survival, India is dealing with a severe yet controllable illness. The difference is significant; it does not warrant complacency but rather calls for calibrated realism. Alarmist narratives risk distorting policy priorities and eroding economic and investor confidence.

At the same time, the present crisis underscores the urgency of a strategic policy response. India must accelerate its energy transition by leveraging the moment to expand renewables such as solar power and green hydrogen, thereby reducing long-term dependence on fossil fuels. It should also move decisively towards expanding strategic storage, not only for crude oil but also for LPG and natural gas, supported by the development of underground storage infrastructure.

Equally critical is the need for trade diversification—lessening excessive reliance on Gulf routes while deepening economic engagement with regions such as Africa, Central Asia, and Latin America. Managing currency risks must also become a priority through the promotion of rupee-based trade settlements and stronger hedging frameworks for importers.

On the industrial front, a shift in policy is required to promote high-value exports and reduce dependence on imported intermediate goods, thereby enhancing domestic resilience. Finally, a robust shipping and maritime strategy is indispensable, involving investment in domestic shipping capacity and strengthened naval capabilities to secure vital sea lanes. In sum, the moment calls not for panic, but for purposeful transformation.

Conclusion

In moments of upheaval, the allure of prophecy often resurfaces. References to Nostradamus’s vision of a “third Antichrist” emerging from the Middle East have reappeared in the context of the US–Israel–Iran conflict. Yet, beyond such symbolism, what is unfolding is a profound geopolitical rupture in West Asia.

Amid this intensifying turbulence, India finds itself at a critical juncture—poised between vulnerability and resilience. The crisis has laid bare structural fragilities: heavy reliance on imported energy, exposure to precarious supply chains, and dependence on external demand. At the same time, it has underscored enduring strengths, including diversified sourcing strategies, robust reserves, and a resilient domestic economic base.

The task ahead is not merely to endure the shock, but to harness it as a catalyst for structural transformation. If India can translate disruption into strategic recalibration, it has the potential to emerge stronger, more self-reliant, and better insulated from the volatility of an increasingly uncertain global order. As President John F. Kennedy pointed out, “When written in Chinese, the word ‘crisis’ is composed of two characters. One represents danger, and the other represents opportunity”.

Storm clouds are gathering; the times are uncertain, and the days ahead will be testing. We watch warily.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma, Chief Economist, Infomerics Ratings is a globally acclaimed scholar. With a brilliant academic record, he has over 350 publications and six books. His views have been published in Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma, Chief Economist, Infomerics Ratings is a globally acclaimed scholar. With a brilliant academic record, he has over 350 publications and six books. His views have been published in Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.