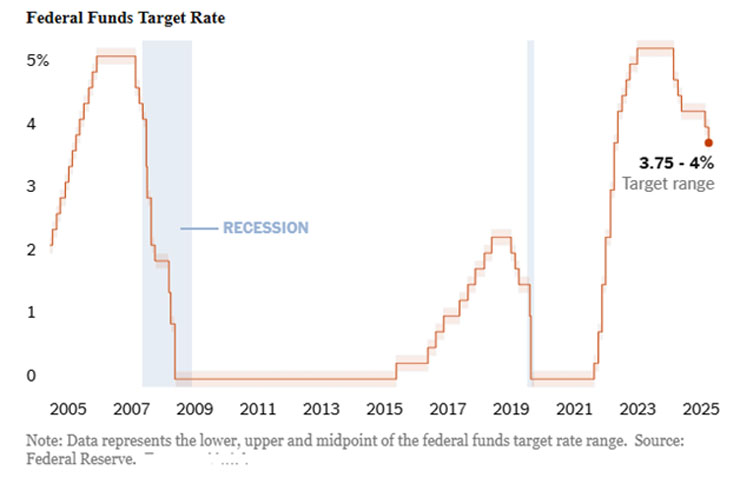

The U.S. Federal Reserve reduced its policy rate by 25 basis points on October 29, 2025, with a 10-2 vote, with newly appointed Governor Stephen Miran wanting to go further in cutting rates this week, and Kansas City Fed President Jeffrey Schmid dissenting in support of no cut at all. on October 29, 2025, citing softening labour-market conditions, increased uncertainty, and weakening growth indicators, despite inflation exceeding the 2% target. This move, which was initiated in the light of a confluence of pain points, marked the second rate cut of 2025, following a similar move in September.

Investors lowered the probability of a cut at the Fed’s December meeting after Jerome Powell, the central bank’s chair, said there were “strongly differing views” on what to do next. Infact, Chairman Jerome Powell justifiably held that further reductions were “not a foregone conclusion.”

Further Cuts Not Guaranteed

The Fed’s statement showed caution: it acknowledged rising risks to growth and employment but emphasized that further cuts are not guaranteed. The decision was also affected by data disruptions from the recent U.S. government shutdown and tight liquidity conditions in financial markets. Additionally, the Fed announced that it would end quantitative tightening (QT), ceasing the reduction of its balance sheet from December 2025, signalling its intent to stabilise liquidity.

Michael Rosen, Chief Investment Officer, Angeles Investments, Santa Monica, CA said, “Investors should expect that inflation will likely run higher for longer, which will limit the degree of additional monetary easing. Equities are down on these remarks as investors had been expecting more rate cuts would provide a boost, but this is a temporary reaction. It is earnings that ultimately drive equities, and those earnings have been strong, and we remain fully invested in our portfolios.”

Mixed Signals

Markets reacted with mixed signals. While the rate cut generally lowers short-term borrowing costs, potentially easing mortgages and business loans, the Fed’s cautious tone dampened expectations of aggressive easing. Interestingly, 10-year U.S. Treasury yields increased, reflecting investor unease over data reliability and policy uncertainty.

From a macro perspective, the rate cut aims to bolster economic activity and employment, though it also raises inflation risks. Ending QT should improve liquidity and support risk assets such as equities and corporate credit, though there is a possibility of market mispricing.

Global Spillovers

Globally, easier U.S. monetary conditions could spur capital flows into emerging markets in search of higher returns, supporting emerging-market currencies and reducing external debt-servicing burdens. Commodity exporters may also benefit from stronger global demand, though a renewed rise in commodity prices could rekindle inflation pressures. Reflecting monetary linkage, Gulf central banks, including Saudi Arabia, the UAE, and Qatar, also cut policy rates by 25 bps.

Implications for India

For India, the move was largely anticipated, but it should improve market sentiment, especially for financials and consumption-driven sectors. Softer U.S. yields make Indian assets more attractive to foreign institutional investors (FIIs), potentially boosting equity and debt inflows. The Fed’s easing also reduces external headwinds, giving the RBI greater flexibility to pause or fine-tune its policy stance.

A milder U.S. dollar could support the rupee, ease external borrowing costs, and reduce debt-servicing pressures. However, if global inflation revives, especially through commodity channels, India may face imported inflation risks, which would limit policy room.

Pathway to the Future

Looking ahead, a December rate cut is not guaranteed. The Fed has reiterated that “incoming data, the evolving outlook, and the balance of risks” will guide its decisions. The coming months may see a synchronised global policy adjustment. Still, emerging markets, including India, will need to navigate domestic inflation, fiscal discipline, and structural reform imperatives amid shifting global dynamics.

ABOUT THE AUTHOR

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.

Dr. Manoranjan Sharma is Chief Economist, Infomerics, India. With a brilliant academic record, he has over 250 publications and six books. His views have been cited in the Associated Press, New York; Dow Jones, New York; International Herald Tribune, New York; Wall Street Journal, New York.